Imagine being told when you bought your plane ticket that there was a 50% chance you wouldn’t get to your destination at all. Would you accept those odds? Planning a retirement can also be like a journey in that you take off once you leave your career. Commonly referenced financial rules offer supposedly helpful guidelines to help you plan better. As a certified financial planner® with 15 years experience, I’ve found that most planning rules are outdated, and even if they work for the average person some of the time, that implies they are wrong about half the time. I believe you deserve better than a 50% chance of landing a successful retirement.

Retirement rules don’t just apply to your finances; they also apply to your expectations about your lifestyle. If you’re like most people, then you probably envision your golden years as being stress free and all about travel and leisure. Research, however, suggests otherwise, which means you need to plan quite a bit differently.

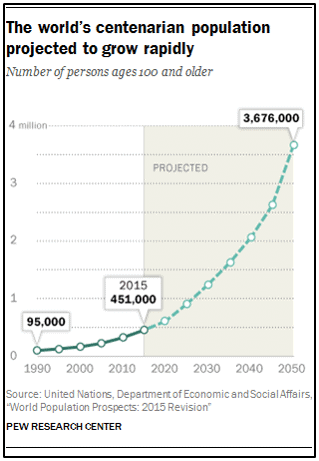

YOU’RE GOING TO LIVE LONGER AND BETTER

The cat’s been out of the bag on this one for a while now, but the commonly referenced life expectancy stats are based on Social Security mortality tables correlate to an average household income of only about fifty-thousand per year. What if your income is above average? Congratulations – your life expectancy goes up. If you also consider the advances we’re making in nanotechnology, biotechnology, and medicine, then it’s not unrealistic to think you might live to age 100 or beyond. Indeed, according to the Pew Research organization, centenarians are the fastest growing age segment on earth.

There is a drastically different mindset between the 65-year old who retires and thinks, “I have another 15 years” versus the retiree who thinks, “I have another 35 years.” So ask yourself, what do you want to do with this chunk of time?

THE GRASS MIGHT NOT BE GREENER

As more and more Boomers enter into the retirement stratosphere, more and more studies are being conducted to help us discover what, really, makes for a happy retirement. Retirement planning researcher Dr. Michael Finke and the Health and Retirement Study (HRS) concludes that money alone does not provide happiness; it’s how you use the money and what you combine it with. Spending time among friends, belonging to a community, and participating in activities that serve a purpose are the true indicators of whether or not a retiree will feel content.

This supports the findings of renowned psychologist Abraham Maslow who developed his Hierarchy of Needs by studying the brightest and most self-actualized among us. Our basic physiological and psychological needs at the heart of this pyramid are either directly or indirectly satisfied by work. If having a job gives us a sense of safety and esteem plus keeps us connected, how will you meet these needs in retirement?

HAVE IT YOUR WAY

Retirement is one of life’s biggest transitions, and it inevitably creates stress. In my experience counseling clients, those that manage the transition the best are not just retiring from something but to something. They have a life plan for this next stage of life. They specify things they want to continue doing, stop doing, and start doing and continually revisit this list.

Married couples especially will want to coordinate their efforts. University of Wisconsin professor Keith Bender reports in his retirement satisfaction findings that while married retirees are better off, if one spouse is still working while the other is retired, friction may result. Women typically have larger social networks than men, so retired men tend to rely more on their wives as their primary source of social interaction. This can cause tension if you’re not planning together.

The bottom line: design the financial component of your plan to support your wants and needs. Most people plan backwards – they start with the money first, and then they make that fit the big picture. That’s kind of like throwing the darts before you hang up bull’s-eye board. Instead of missing the mark, make sure that your financial plan starts with you.

_______________________________________________________________________

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent registered investment advisory and wealth management firm specializing in retirement, tax, and investment planning.