by Kevin Kroskey, CFP, MBA

When the term “retirement planning” is used, most think of the financial aspects of retirement myopically through a material lens. However, the social, emotional, and physiological stresses that transitioning into and throughout retirement impose are much more difficult to deal with. These issues get to the core of oneself. Socrates’ maxim “Know Thyself” applies greatly to retirement. The better you know yourself the better you will be able to relate to others, manage your emotions, and manage your wealth whether in a material sense or otherwise.

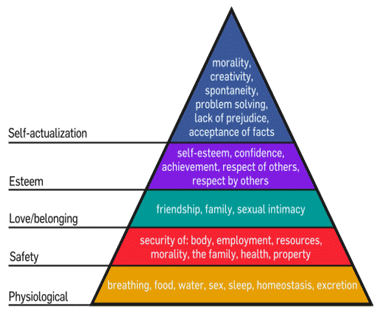

Maslow And Retirement

“Self actualization is the desire to become more and more what one is, to become everything that is capable of becoming.” – Abraham Maslow

Maslow’s Hierarchy of Needs illustrated in the pyramid relates very well to work and to retirement. At the base of the pyramid essential needs are met from work by bringing home a paycheck, having secure employment, and having fruitful relationships with others at work. Esteem needs are met through work via achievement, recognition, and respect received.

When you take work out of the equation, these needs still persist for oneself but must be replaced in a non-work environment. For example, rather than bringing home a paycheck as you did for the last thirty or forty years, you now must produce a paycheck from accumulated assets, pensions, and Social Security. Rather than having your work friends where work was the common thread that brought you together, you need to more fully develop friendships now in a non-work setting. And rather than having your esteem needs met by doing a good job at work and receiving recognition and respect for it, you need to refocus your purpose to have these esteem needs met in a different manner.

When reflecting on the benefits one receives from work, it is no wonder that many baby boomers today say they would like to continue to work in some fashion in retirement. It is also no wonder that the people that often have the most difficulty in making the retirement transition are the ones that were most successful at work.

These successful people most often devote a significant portion of their life and purpose to work. For the executive or entrepreneur that directed considerable amounts of energy towards work and had significant responsibilities and purpose, that energy does not simply go away. Rather the energy could easily be redirected and now focused within the household, causing marital or family stresses.

Three Questions

Proper life planning can be done to more effectively manage life transitions. George Kinder is often recognized as the father of the Life Planning movement. Life Planning describes this more holistic and integrated view of financial planning. Kinder is famously known for his ‘Three Questions:’

Question One: Imagine you are financially secure, that you have enough money to take care of your needs, now and in the future. How would you live your life? Would you change anything? Let yourself go. Don’t hold back on your dreams. Describe a life that is complete and richly yours.

Question Two: Now imagine that you visit your doctor, who tells you that you have only 5-10 years to live. You won’t ever feel sick, but you will have no notice of the moment of your death. What will you do in the time you have remaining? Will you change your life and how will you do it? (Note that this question does not assume unlimited funds.)

Question Three: Finally, imagine that your doctor shocks you with the news that you only have 24 hours to live. Notice what feelings arise as you confront your very real mortality. Ask yourself: What did you miss? Who did you not get to be? What did you not get to do?

These questions get progressively more difficult to answer and aim to get to the core of oneself—knowing who you are as a person and stripped away from the job that you do nearly every day.

Tying It All Together

You may be reading this and wondering, “What does this have to do with money?” Yet, it has everything to do with money. You can prioritize your needs and construct a plan to have the utmost confidence that your essential needs be met regardless of economic or life events. If markets don’t cooperate and returns are lower than expected, you have a predetermined plan to adjust your spending on those things that are less essential to you and your values.

When you understand what you want to do with your life, you can make financial choices that reflect your values. You can focus your consciousness on the things that matter most and achieve clarity and confidence while disregarding unimportant items. This clarity and confidence will correlate directly to making smart financial decisions rather than emotionally driven ones that often punish less confident, less focused investors.

Retirement planning is obviously much more than a financial event even though finances are certainly a part of it. Life planning is not an event either. This is about process. It starts with being mindful and aware and continues with deciding and re-deciding.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists families with their overall wealth management, including retirement planning, tax planning and investment management needs.