by Kevin Kroskey, CFP, MBA

Anyone studying the long-run history of American business cannot help but observe how many of the prominent firms of one era fail to make it to the next. Market economies are characterized not only by intense competition but also by disruptive change. Sometimes a company’s toughest competitor turns out to be a firm it has never heard of selling a product or service that didn’t exist until recently. The list of companies that once dominated their industry but have fallen on hard times is lengthy enough to give every thoughtful investor reason for sober reflection.

Creative Destruction Drives Change

Among many possible examples, a number of firms come to mind that were once highly regarded but later encountered serious or even fatal problems.

Bethlehem Steel pioneered the steel I-beam, which launched a skyscraper boom in cities across the country. Its engineering expertise supplied the steel sections for the Golden Gate Bridge. But growing competition and a changing marketplace eventually took their toll, and the firm filed for bankruptcy in 2001.

In 1973, Eastman Kodak held a seemingly impregnable position in the lucrative market for photo film and chemicals, enjoyed a reputation for innovation and astute marketing, and boasted a market value even greater than oil giant Exxon. Kodak shareholders had been favored with an uninterrupted stream of dividends dating back to 1902. Today the company is struggling to reinvent itself as the film business shrivels, the dividend has been suspended, and the share price is limping along under $3.

A Fortune article profiling Pfizer in mid-1998 praised it for having “one of the richest product pipelines in the Fortune 500.” In early 1999, a Forbes cover story sounded a similar note, crowning Pfizer “Company of the Year” and observing that “the people who brought us Viagra have more blockbusters on the way.” Thirteen years later, the Viagra boom has subsided, patents are expiring on highly profitable products, and the gusher investors expected from the research pipeline has slowed to a trickle. The share price has slumped over 50% since year-end 1998 compared to a 3% loss for the S&P 500 Index.

Some companies almost single-handedly create new industries but still find it difficult to turn innovation into a permanent advantage. Pan Am (air travel), Kmart (discount retailing), Polaroid (instant photography), and Wang Laboratories (word processing) all had impressive initial success and provided handsome rewards for their investors. Kmart, Polaroid, and Wang Laboratories were all cited as examples of “excellent” companies in the 1982 bestseller In Search of Excellence. Alas, neither Pan Am nor Polaroid survives today, and Kmart shareholders were wiped out when the firm emerged from bankruptcy in 2003.

Evidence of this “creative destruction” appears all around us. Shares of Minnesota-based Best Buy Co. slumped to their lowest level since 2008 after reporting a 30% drop in profits for the third quarter of 2011. For most of its life, Best Buy has been the toughest kid on the block, vanquishing rivals such as Highland Superstores and Circuit City on its way to becoming the nation’s leading electronics retailer.

Will Best Buy fall victim to even tougher competitors such as Amazon.com or Wal-Mart? Or is this current downturn just a speed bump on the road to even greater success? No one can say. For every riches-to-rags story, we can find another tale of decline followed by dramatic recovery. According to some accounts, for example, Apple was only a few months from bankruptcy when Steve Jobs returned to the company in 1997. Now it vies with ExxonMobil for the number one spot in a ranking by market cap. And who would have imagined that a floundering New England textile firm with a low-margin business that sells suit-lining fabric would one day become a financial colossus known as Berkshire Hathaway?

Implications for Investors

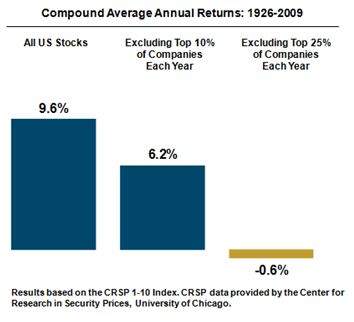

The potential cost of choosing the wrong companies can be severe. Much of the return of the markets comes from just a few stellar performers each year. If you do not own these performers, returns will suffer. As seen from the chart, missing the top 10% of companies each year would cause investment returns to shrink from 9.6% to 6.2% over the sample period. Missing the top 25% causes returns to go negative.

The potential cost of choosing the wrong companies can be severe. Much of the return of the markets comes from just a few stellar performers each year. If you do not own these performers, returns will suffer. As seen from the chart, missing the top 10% of companies each year would cause investment returns to shrink from 9.6% to 6.2% over the sample period. Missing the top 25% causes returns to go negative.

The thrill of owning a great growth company during its most lucrative phase is a powerful incentive to search for the Next Big Thing. But almost every company with a highly profitable position is under constant attack from competitors seeking to garner a portion of those hefty profits for themselves.

As a result, the search for firms destined to generate greater-than-expected profits for many years into the future is fraught with peril and likely to end in frustration at best and financial ruin at worst. Most investors will be far better off harnessing the forces of competitive markets and putting them to work on their behalf by holding a diversified portfolio, comprised of many thousands of stocks. As Nobel laureate Merton Miller once observed, “Above-normal profits always carry with them the seeds of their own decay.”

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.