The most commonly held belief about how and when to file for Social Security basically boils down to a ‘get it while you can’ strategy. In the past I’ve talked about how many of these commonly held beliefs or referenced rules for financial planning are not only outdated, but harmful to the long-term success of your retirement. Filing for Social Security, however, has the heightened challenge of being quite an emotional decision for many.

Forty-two percent of Boomers expect to see their benefits reduced at some point during retirement, and Boston College’s Center for Retirement Research reports that in 2013, more than a third of those age 62 claimed their retirement benefit as soon as they could. Because the fear of running out of money is also on most people’s minds, no one is too keen on the idea of withdrawing from their savings while waiting to file. Yet the reality is that filing early locks in a lifetime of reduced benefits – up to 30 percent. For married couples utilizing a spousal benefit, the penalty for filing early is even steeper – up to 35 percent.

Entering into retirement and filing for Social Security seems to be linked in most people’s minds, but I’d like to make the case here for employing a more strategic approach. By waiting to file, you stand to gain:

- a higher inflation-adjusted income stream

- more spendable income over your lifetime

- insurance against living too long

- increased tax-planning flexibility

- a lower long-term withdrawal rate on your portfolio

FACING THE FEAR

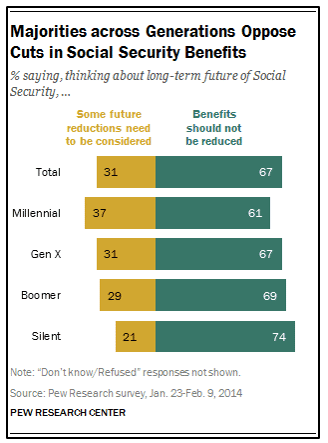

Let’s first address this belief that the system is going broke. Social Security has enough funds to pay full scheduled benefits until the year 2035, at which point either payroll taxes will need to be increased or benefits reduced by 13 percent. This will only happen if no changes are made to the system.

Also consider that the last material amendment made to Social Security in 1983 disproportionately affected the benefits of younger workers – people born in 1960 or later. These folks were only 23 years old when full retirement age was changed from 65 to 67, and they had their entire careers to plan for this change. It’s likely that any future changes to the system will be similarly phased-in.

Some people also worry about not living long enough to reap the full rewards of their benefit if they file later. The breakeven point for many people is in their early 80s. These ages are well below the joint life expectancy – when the second spouse will pass – for an average married couple entering retirement today. Since the higher of the two Social Security benefits will be paid as long as either spouse lives, delaying at least the larger benefit often makes sense.

UNDERSTANDING THE BENEFITS

Is Social Security insurance against living too long, or is it another asset on the family balance sheet? When it’s used properly, it can be both. Each year that you delay gratification (up to age 70) your benefit grows. The actuarial adjustments that the Social Security administration uses to calculate benefits haven’t been updated since 1983. In the meantime, interest rates have decreased while life expectancies have increased. This combination means that delaying your benefit can be a great deal.

I find that many successful families do not pay enough attention to the claiming decision. Yet they often can benefit the most, since they have paid more into the system, have higher benefits, and longer life expectancies. I’ve advised on many cases where an improved claiming strategy for a successful married couple regularly yields more than $250,000 more in expected lifetime spending versus filing early.

Delaying Social Security gives you a higher level of income over time, but you first have to get over the hurdle of spending more of your investment money upfront before the benefit begins. It might help to keep this in mind: delaying Social Security doesn’t mean that you have to spend less early in retirement and more later on. Quite the contrary, if you employ a well-designed filing strategy, then you can afford to spend more over the entirety of your retirement from day one. You owe it to yourself to get the most from what you paid in.

————————————————————————————————————-

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent registered investment advisory and wealth management firm specializing in retirement, tax, and investment planning.