by Kevin Kroskey, CFP, MBA

With the strained balance sheets of governments in the Europe and US being the focus of so much media and market attention in recent times, it is understandable that investors would fret about the credit risks of putting their money into sovereign bonds. Countries can and have defaulted on their debt. As recently as 2010, Jamaica defaulted on its debt. Others to default in the past decade have included Ecuador (2008), Belize (2006), Dominican Republic (2005), Uruguay and Nicaragua (2003), Moldova (2002) and Argentina (2001).

Markets incorporate information—economic variables, credit ratings, risk perceptions, willingness to pay—and put a price on them. So what are the markets telling us of sovereign bonds?

Conflicting Information

How does a country like France, with total government debt of nearly 70 percent of its economic output, maintain a top tier ‘AAA’ bill of health from all the major credit rating agencies—Moody’s, Standard & Poor’s and Fitch?

Correspondingly, how does a country like Japan, with an even bigger proportionate debt load (184 percent of GDP) than beleaguered Greece (148 percent), maintain a superior credit rating (AA/AA–) to the junk paper of the Greeks (CCC/CC)?

And how does the United States—supposedly the safest of all safe havens—hold a AAA/AA+ credit rating when it has the biggest nominal debt load of any country at nearly $15 trillion or just over 60 percent of its economic output?

Credit Ratings & Market Prices

There is a very large market in a form of derivatives called ‘credit default swaps’ or CDS. These are a form of insurance against the possibility of default. This very liquid market serves as a useful guide to how the market views the relative risk of default among borrowers. It is clear that risk as judged by the market and the risk as judged by credit rating agencies are not necessarily the same.

For example, seven months before it defaulted in 2008, Ecuador was rated ‘BBB’ by Standard & Poor’s. Yet, its bonds were yielding around nine percentage points above those of US Treasury bonds, which implied a risk associated with a ‘CCC’ rating, according to a report by the International Monetary Fund. This disparity is not a one-off quirk either.

Broadly speaking, the higher the price of default insurance for each sovereign borrower, the greater the market perceives the risk of investors not getting their money back. Not surprisingly, the most expensive CDS—as of August 2011—were those for Greece, which also happened to be the lowest rated country in this sample. The least expensive CDS were for Norway, a AAA-rated borrower with a low debt burden. So far, so good.

But now consider the US, which was downgraded by S&P, but whose cost of default insurance was lower than that of France, which maintained a AAA rating at time of writing. Or Mexico, with the lowest investment grade rating of ‘BBB’, whose default insurance actually cost less than AA-rated Spain.

The point of this is that the market believes the US, while fiscally challenged, retains sufficient flexibility to raise funds if needed. On the other hand, some of the European borrowers—locked into the monetary settings and debt constraints of the European Union—were seen by the market as having less flexibility.

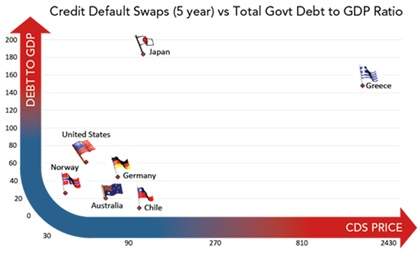

Debt-to-GDP & Market Prices

If the rating agencies don’t necessarily serve as a good guide in assessing sovereign credit risk, what about considering total debt-to-GDP ratios? The chart shows seven countries with their total debt-to-GDP ratio and the price of their individual credit default swaps as of August 2011.

Again, Greece was the most expensive country to insure and Norway the cheapest. But then look at Japan, whose total debt in proportionate terms is the highest of them all, but whose CDS were only marginally more expensive than those of Chile—the least indebted of all these seven nations. Australia, which is one of the least indebted sovereigns in the developed world, was judged by the market as actually a higher credit risk than the US.

Implications for Investors

In pricing risk, it is usually better to give greater weight to market signals—if for no other reason than the price represents the combined wisdom of millions of market participants staking real money on the outcome. While credit ratings and debt-to-GDP ratios are important, the market ultimately judges sovereign risk on both the perceived ability of sovereign borrowers to find new sources of revenue as needed and the perceived willingness of those borrowers to repay. So while the US undoubtedly is stretched, it is perceived by the market as having the capacity to fund its liabilities through tax increases and/or additional spending cuts. It also has the advantage of being able to borrow in its own currency in capital markets and is less reliant than the Europeans on bank funding.

For investors, the way to deal with these risks are the tried and true methods of working with the market, diversifying broadly, taking risks only when there is a demonstrated reward for doing so and basing one’s strategy on a long-term, scientifically proven research and a consistent philosophy.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.