Recent headlines surrounding bank failures may have you wondering: How safe are my investments? How does FDIC insurance work with my investment accounts? What happens if my custodian – Fidelity, BNY Mellon / Pershing, Schwab, TD Ameritrade – becomes insolvent like Silicon Valley Bank (SVB)?

It’s important to remember that market risk stems from fluctuations in the value of the investments you hold. When investments lose value there is no insurer or government entity to step in to make you whole. Market risks such as lending to governments or companies (aka buying bonds) or investing in a company’s equity and share of profits (aka owning stock) are risks you take to participate in market gains.

A lesser-known type of risk investors take is custody risk. This is the risk of incurring a loss due to the custodian’s insolvency, negligence, fraud, or inadequate recordkeeping. Before diving into what safeguards are in place for your investments, it is crucial to differentiate bank deposits from investments held by a custodian.

Bank Deposits

When money is deposited at a bank, this deposit becomes a general liability of the bank. The bank promises to pay back your deposit in the future. You can think of this as lending money to the bank. While most don’t think of their cash at a bank as a loan, SVB provides a stark reminder that you should.

To make money, the bank takes this deposit and lends it to other customers in the form of mortgages, car loans, etc. These loans then become an asset of the bank. The goal of the bank is to make more money on its assets (loans) than they pay on its liabilities (your deposit).

In the case of a bank failure, the FDIC guarantees up to $250K of deposits. In the case of SVB, the government has guaranteed all deposits, including those above the $250K threshold, largely to try to avoid similar issues from occurring at other banks.

Custodian-Held Investment Accounts

When you hold investments with a qualified custodian, your investments are held in a segregated account and do not become a liability of that custodian. Further, they are not used by the custodian in the same manner as bank deposits are in being loaned to other customers. Due to these distinct and important differences, investors cannot lose money in the same manner as bank depositors if their custodian becomes insolvent.

In addition, most custodians utilize a money market fund as the cash-equivalent vehicle in an investment account. This keeps any cash maintained at the financial institution segregated from the general fund of that institution.

Perhaps you are wondering: if I cannot lose money if my custodian becomes insolvent, then how did Bernie Madoff’s clients lose money?

Bernie Madoff was committing fraud for many years and did not have a third-party custodian like Fidelity, Pershing, Schwab, or TD Ameritrade. Rather, he pooled customer assets and commingled them with his company’s assets, which more easily enabled the fraud. Yet, these investors and victims of fraud were ultimately protected up to $500K per account ownership category. Any amount above that threshold was only paid back to investors as funds were recovered.

So what protects you from fraud, negligence, or inadequate recordkeeping within investment accounts? Investments are not protected by FDIC insurance but are instead protected by the Securities Investor Protection Corporation (SIPC) for member firms. Investments are covered up to $500K ($250K max on cash) per account ownership category. Therefore, if you have 4 accounts, each within a different ownership category (individual, joint, Roth IRA, IRA), each account is protected up to $500K. SIPC covers money market funds up to the $250K threshold as they are considered securities.

Now you are thinking $500K may not be enough when dealing with higher net worth individuals. If I have more than $500K in an account at a custodian, am I at risk?

Most large, well-known custodians (and all custodians utilized by True Wealth on behalf of clients) maintain what is called Excess SIPC insurance. This coverage, typically $600M to $1B in aggregate extra coverage, provides protection above the SIPC limits. There is no per-customer limit, but there is usually a limit on the protection of cash, generally over $1M.

With the above safeguards, along with SIPC and excess SIPC insurance, most failures within the investment industry do not affect customers. One of the best examples is that segregated investment accounts at Lehman Brothers were fully recovered after Lehman’s bankruptcy during the Great Financial Crisis (GFC).

(Note: BNY Mellon, which wholly owns Pershing, has an additional designation post-GFC of being a Globally Systemically Important Financial Institution — just one of thirty such institutions as of November 2022 — that is more colloquially referred to as “too big to fail.”)

Fund Structure Protections

While you may hold a mutual fund or exchange-traded fund (ETF) with a custodian, and the custodian holds these assets in a segregated account, the fund structure provides additional safeguards.

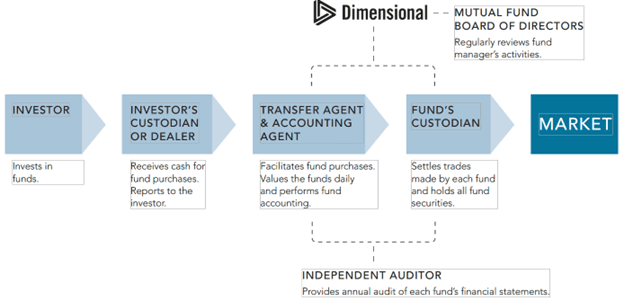

A mutual fund company is structured differently than other companies and typically has no employees in the traditional sense. Instead, funds hire providers to carry out investment and business activities. For example, a mutual fund employs an investment adviser (think Dimensional Fund Advisors, Vanguard, Blackrock, etc.) to decide which securities to buy and sell, consistent with the fund’s investment objectives. These trades are completed by a separate entity — the fund custodian that is distinct from the custodian where your account is held — who takes possession of securities purchased or transfers securities sold. The investment adviser never handles securities in a trade. This separation between management and custody is mandated by securities laws and is intended to help prevent the fraud-based losses that have occurred in less-regulated investment products.

Most mutual funds use qualified banks as custodians, and the banks are required to segregate (there’s that magic word again!) mutual fund securities from other assets. In the event that a mutual fund ceased operations, the securities would remain with the custodian while the fund’s board of directors decided whether to hire another investment adviser or sell the securities and distribute the proceeds to shareholders.

Mutual funds may engage a transfer agent to help facilitate new investments or an accounting agent to value securities. Oversight for many of a mutual fund’s operations is provided by a board of directors. Mutual funds are required to maintain a board that meets regularly, and a majority of the directors must be independent of the mutual fund company. The board is responsible for approving the hiring of a chief compliance officer (CCO). The CCO implements and oversees written policies designed to prevent securities law violations by the mutual fund. The CCO reports regularly to the full board and separately to the independent directors and can be replaced only with approval of the full board.

Below is a helpful diagram from Dimensional Fund Advisors:

There has been a lot of misinformation regarding and uncertainty caused by the recent bank failures. Markets discount when uncertainty exists. Expect volatility to continue. We’re here if you need help or have questions.

Aaron Seil, CFA & Kevin Kroskey, CFP®, MBA | March 2023

PS: If you’re ready to explore a relationship, use this link to schedule a free 15-minute call with one of our experienced and credentialed professionals.

See also:

Fidelity: Safeguarding Your Accounts

BNY Mellon | Pershing: Strength & Stability

Federal Reserve Announcement on SVB

Lehman Brothers Bankruptcy Ends 09/28/2022

Red Flags of Investment Fraud | True Wealth Design August 2022