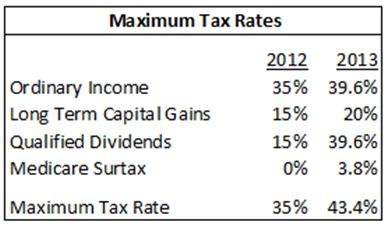

At the start of next year, America’s entire tax regime is set to change, as the Bush-era tax rates shift back to their previous (higher) levels and preferential (lower) rates on capital gains and dividends phase out. The estate tax rates will go up and the exclusion amounts will go down. Congress may intercede between now and then, but in an election year, any meaningful compromise is far from certain.

This has created an unusual level of uncertainty. However, the recent Supreme Court ruling on the 2010 Patient Protection Affordable Care Act (sometimes colloquially referred to as “Obamacare”) has taken one uncertainty off the table. We now know that a new tax will have to be planned for as of January 1. As a way of shoring up the shaky finances of our Medicare Trust Fund, the budget reconciliation bill that was passed in conjunction with the health care reform bill will impose a 3.8% Medicare Surtax starting in tax year 2013.

What does that mean to you? For 97% of all households–individuals whose current taxable income falls below $200,000, or couples with a joint income below $250,000–the tax is irrelevant. It only applies to persons above those income thresholds. Yet, this new tax is not indexed for inflation and will thus be applied to more people over time.

People whose income does exceed those thresholds will pay the 3.8% tax on the lesser of an individual’s net investment income for the year or adjusted gross income in excess of the threshold amounts. Net investment income is how much you made, in aggregate, on taxable interest, dividends, distributions from annuities, royalties, net rental income, income from passive investments like partnerships, from actively trading financial instruments and commodities, plus the gain from selling non-business property. Of course, you get to subtract out losses and expenses related to those investments.

So, for example, suppose a husband and wife had adjusted gross income of $400,000 in 2013. The first number that the 3.8% tax might be applied to is $150,000 ($400,000 – $250,000). Moving to the second test, let’s suppose that they earned interest income amounting to $40,000, and had sold some stocks for a capital gains profit of another $40,000. But they had also sold some stocks at a loss, amounting to $15,000. Their net investment income comes to $65,000. That’s obviously lower than $150,000, so that is what the couple pays the Medicare Surtax on. The tax comes to $2,470.

You might have read that this tax will be imposed on the gains from the sale of your house, but that will generally not be true for most. If your income is above the threshold limit, you and your spouse would still have to make a profit of more than $500,000 ($250,000 for singles) on the sale of your house before the tax becomes applicable.

The investment calculation does not include payouts from a regular or Roth IRA, 401(k) plan, or Social Security, or any income from a business on which you are paying self-employment tax. It also doesn’t apply to the appreciation of your stocks or mutual funds until or unless they’re sold and gains are taken. However, IRA and qualified plan distributions do raise your modified adjusted gross income, and this, of course, can put you over the threshold.

Because the amount of investment income determines, in part, your total income, this is one tax that is rich with planning possibilities. Asset location, where income-producing assets are held in tax-deferred accounts and more growth-oriented investments are held in after-tax accounts, will yield even greater benefits. If after-tax assets comprise a much larger percentage of an investment portfolio than tax-deferred assets, tax-free municipal bonds can be used in after-tax accounts, as their income isn’t affected by the surtax.

A potentially highly impactful strategy to maximize after-tax wealth is to convert IRA assets to Roth IRA assets in 2012, and pay the taxes with money from after-tax assets. Distributions from the Roth IRA never show up in any of these 3.8% calculations, and the money paid up-front in taxes lowers the taxable income amounts in the future. As a potential bonus, the tax rates in 2012 might be lower than they would be if all the tax rates jump on January 1.

For those who are charitably inclined, accelerated gifting to a donor-advised fund can help reduce income below threshold amounts while retaining control over the gifted assets. Charitable trusts are more complicated but can also be effective tools to consider.

It is important to remember that taxes are only one component of your total investment picture. The tax-tail should not wag the dog. Rather than having a strategy that simply tries to lower your payments to Uncle Sam, having a proactive strategy to maximize after-tax wealth over time will be the best one for your personal financial needs and for building retirement income.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs. Kevin can be reached via email at kkroskey@truewealthdesign.com or by phone at 330-777-0688.