At the Berkshire Hathaway annual meeting in May, 2009, a slide depicted a trade ticket from December 19, 2008, showing a Berkshire sale of $5 million of Treasury bills. They were coming due on April 29, 2009. Berkshire sold the bills for $5,000,090.70. If that buyer had instead put their money in a mattress, by April 29 they would have been $90.70 better off. Buffett said: “We may never see that again in our lifetimes.”

In June, investors were so risk averse that this has happened yet again. Investors were willing to pay the German government to look after their money; not a risk-free return, but a return-free risk. Yields on two-year German notes sank to an all-time low of -0.005% on June 1. Looked at another way, anxious investors were prepared to accept a negative return for the comfort afforded them by parking their cash with the German government. And this was even before taking inflation into account.

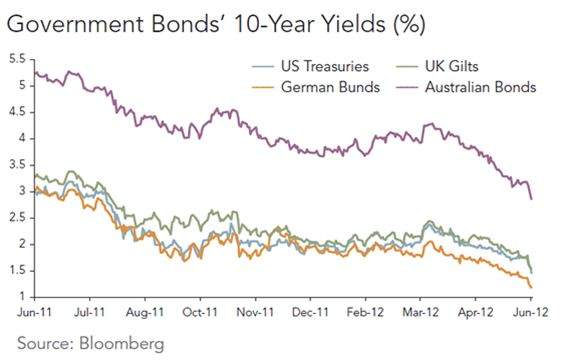

The extreme state of risk aversion in global markets is reflected not only in German bunds. In the US, Treasury bond yields have hit record lows, as have their equivalents in Australia, the UK, France, Austria, Finland, and the Netherlands.

The causes of this mass shying away from risk are well documented: worries that the Eurozone will break up, concernthat the US economic recovery is stalling, signs of a slowdown in China, and a loss of momentum in emerging markets. Anyone who takes note of media and market commentary will know that there are a wide range of opinions about the likely outcomes of these issues. The important point for the ordinary investor is that all those opinions and uncertainties are already reflected in current prices.

Here’s how this process works: Security prices are an expression of the market’s aggregate view of future expected cash flows divided by a discount rate (or risk premium) that investors demand for putting their money into risky assets.

When the price of a security falls, it can be due to lower expected cash flows, a higher discount rate, or a combination of the two. While we don’t know the exact mix of these influences, we do know that if lower prices are wholly due to lower expected cash flows, expected returns will be unaffected. On the other hand, if lower prices are due to the application of a higher discount rate because of higher risk aversion, we can say expected returns for the risky assets are higher.

Investors’ willingness to pay to park their money in German bunds or US Treasuries at record-low yields is an indication of higher risk aversion. Higher risk aversion should be linked to higher discount rates, so the probability is that expected return premiums on risky assets have gone up.

Think back to what we saw coming out of the first stage of the financial crisis in March 2009. Risks were high, and prices of risky assets went down. Many investors, overcome by the uncertainty at that time, sought refuge in government bonds. Due to this generalized increase in risk aversion, investors demanded a higher premium before putting their money into equities and corporate bonds. But as risk appetites revived that year, those risky assets paid a very substantial return. Share prices rebounded, and the yield spread of corporate over government bonds narrowed sharply.

The takeaway is that sheltering in what are perceived as the safest government bonds may provide certainty for a time, but also comes at the cost of forgoing the significant increase in risk premiums that may be available.

This is not to argue that increasing one’s allocation to risk-free assets is never a legitimate decision. Such a course may well be appropriate for the individual investor, based on his or her own risk preferences, liquidity needs, and investment objectives. If funds are needed for short-term cash flows, these funds should not be invested in longer-term and more volatile investments. If possible, however, it is best to develop appropriate asset allocations for individuals based on their risk tolerances outside these periods of distress. That’s because emotionally reacting to the markets and selling risky assets at such times can be very expensive.

In summary, it is worth reflecting on the fact that record-low yields on government bonds, and in particular negative yields on the safest assets, may be an indication of extreme risk aversion and high discount rates on risky assets. This higher discount rate would have been partly responsible for their recent price decline and will probably be reflected in higher expected returns.

When risk appetites return—and you cannot know for certain when or if that will happen as we are talking about “risk”—those risky assets may stage an equally dramatic recovery. Seeking to time those changes can be a very, very expensive exercise. So at times like these, it’s worth reminding ourselves that safety comes at a cost.

The worrying events of recent weeks and months are incorporated into prices. But remember that future events, unknown to us today, can always affect prices in positive or negative ways beyond the expectations built into the market today.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.