Social Security’s future solvency is a regular discussion point when considering your retirement planning. It is common to think your benefit will be reduced from what is shown on your statement. Yet, that position is often taken without good information or critical thinking. Below is relevant information from the 2019 Trustee’s report along with a historical perspective to serve as a more informed guide. We also included some comments on what we believe are most likely reforms.

Funding

Until 2011, the Social Security system collected more revenues than it paid out and that has been generally true since the 1940s. Most Social Security benefits are simply a transfer of collected payroll taxes paid to benefit recipients. When a surplus existed, it had been used to pay government operating expenses, and for decades, the government issued “special issue federal securities,” which are fancy IOUs that pay interest, to the Social Security trust fund.

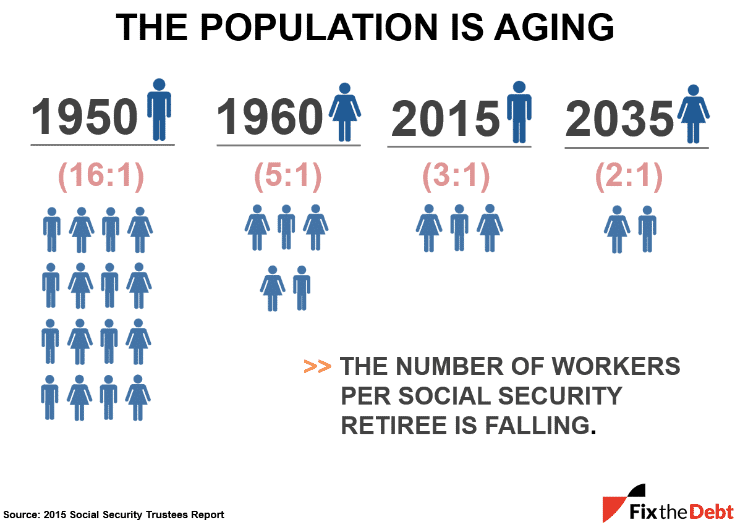

In 2011, Social Security crossed that threshold where benefit payments exceeded the amount collected. Why? Because fewer people are paying in relative to the number that are receiving benefits. In 1950, there were sixteen workers paying into Social Security for every beneficiary. By 2035, that ratio is projected to fall to about 2:1.

When actuaries crunch the numbers for these projections, they consider estimated rates for population growth, longevity, as well as wage and economic growth. Projections show if nothing is done to fix the system, the trust fund will run out of reserves – fancy IOUs – in the year 2035.

At that time, only money collected from current workers would be available to pay Social Security beneficiaries. That means the beneficiaries would, in 2035, see their payments drop to about 75% of what they were promised. I’d suggest this becomes a worst-case scenario.

Past Is Prologue?

In the late 1970s, Social Security was also running deficits that were depleting the trust fund with insolvency looming in 1983. In response, President Reagan signed an amendment in 1983 pushing back the full retirement age from 65 to 67, phased in by birth year. Age 67 as full retirement age started for those born in 1960 and later. Thus, when Reagan made the changes in 1983, someone born in 1960 was 23 years old and had more than 40 years to plan for the change.

What is most interesting is that actuarial calculations at the time suggested the 1983 reforms were anticipated to provide solvency for another 50 years. So, this means the trust fund depletion, projected for the mid-2030s is right on track after 35 years. Kudos to you, government projectors.

No doubt additional reforms are required to ensure solvency longer-term. It is my opinion, based on more common proposals and considering the amount of the projected deficit, that these changes are most likely going to come in the form of 3 changes: (1) increasing the percentage high income earners pay into the system, (2) further pushing back the full retirement age, and (3) modifying the cost of living adjustment to “chained CPI” (historically about 0.25% less than CPI). With these likely changes, younger, highly compensated workers will be disproportionately affected and not those nearer retirement.

Chained CPI made it into the tax code with the 2017 tax reforms and has previously garnered bipartisan support. This change may seem negligible but becomes material over time and will affect everyone planning for retirement.

If you are nearing retirement and still concerned about how solvency may affect your retirement, considering a worst-case scenario of 75% of promised benefits along with lower cost of living adjustments is a reasonable starting point.

See Also: