Have you acquired stock over time and seen it significantly rise in value over time? Perhaps you simply bought and held, were gifted shares, inherited stock through a credit shelter trust, or accumulated company stock through grants or options. Now you have large, embedded capital gains and a more concentrated portfolio.

What should you do? Let it ride? Or should you sell, pay taxes, and reinvest in a more diversified portfolio?

In Part 1, we discussed the issues with having a concentrated stock position and the benefits of a more diversified one. A case study showed selling the concentrated position outright, paying the taxes, and investing after-tax proceeds into a diversified portfolio can vastly improve your expected wealth after taxes looking out a few years.

An astute reader may have thought, “Well I’m going to hold these low-cost basis stocks until I die. Then all the income tax obligations go away (aka basis is stepped-up at death). So, your example doesn’t apply to me.”

Touché. Let’s now investigate this case mathematically.

Sell Vs. Step Up

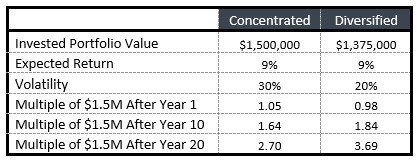

We will use the same numbers as in part 1. You have a $1.5M concentrated portfolio with a cost basis of $1M. If you sell and obtain a diversified portfolio, you will have $1.375M to invest after paying taxes at a 25% rate. We presume both portfolios have the same 9% expected return. (Recall this is an overly conservative assumption in favor of the concentrated portfolio.) Importantly, the concentrated portfolio is more volatile than the diversified one.

In the table you can see the growth of wealth after 1, 10, and 20 years for both portfolios. This multiple is based on the expected future value of the portfolio – the 50th percentile outcome – divided by the Initial Portfolio Value of $1.5M.

For example, the Diversified portfolio can be expected to be $5.535M after 20 years (3.69x multiple of $1.5M) and the Concentrated portfolio $4.05M (2.70x multiple). If death were to occur at this point, unrealized gains go away for both portfolios, and the Diversified portfolio delivers $1.485M more to your beneficiaries. This is despite having $125,000 less invested from the start due to paying taxes to diversify. Drawing from the table, you can expect to be better off for you and your heirs within 10 years or by age 70.

Other Considerations

Emotions are real. No one likes to pay a large tax bill, and you may have to overcome some sort of sentimental attachment to the stock that brought you these gains. But always start with logic and math. Then be pragmatic and consider emotions. Perhaps you sell a portion but not all of the concentrated holdings or have a plan to transition it all over the course of a few years.

In terms of the math, what if your gain is significantly higher than the 50% gain illustrated in the table? What if you can expect a higher return from the diversified portfolio, which is quite reasonable after all?

Alas, you and your situation are snowflakes. Thus, you must run your numbers and rationally execute the plan or have a trustworthy and competent financial professional do so for you. And while this may seem complicated, as Einstein said, “Everything should be made as simple as possible, but not simpler.”

In part three of the article, we’ll consider strategies that may further improve the results of the diversified portfolio.

Should I Sell a Stock with a Large Taxable Gain? (Part 1) – True Wealth Design