Have you acquired stock over time and seen it significantly rise in value over time? Perhaps you simply bought and held, were gifted shares, or accumulated company stock through grants or options. Now you have large, embedded capital gains and a more concentrated portfolio.

What should you do? Let it ride? Or should you sell, pay taxes, and reinvest in a more diversified portfolio?

Concentration Risks

Famed economist and Nobel Prize winner Harry Markowitz called diversification “the only free lunch” in investing. It is a powerful tool to manage risk and to systematically capture stock market returns.

A simple example may help illustrate this. Consider the return of the S&P 500 index in 2020. The index as a whole produced a solid 18.4% return for the year. However, unless you were invested in all 500 stocks within the index at market weightings, your returns could have varied significantly from this number. More than one-third of the stocks within the index posted negative returns and 50 companies down more than 25%. On the flip side, only 37% of the stocks outperformed the index with eleven stocks rising over 100%.

The median return or the return on the 250th best performing stock in the 500-stock index was only 9.72%, barely half of the index return.

Looking longer-term, the annualized return from 1994 through 2020 for all U.S. stocks was 10.3%. However, that return dropped to 6.3% after excluding just the top 10% of performers each year and to negative 1.6% after excluding the top 25% of performers.

The only way to ensure you are selecting the top stocks that deliver much of the market return is to own them all.

Optimizing After-tax Wealth

While diversification has many important benefits, you may have a preference to stay put in your portfolio. After all, why not avoid the capital gains taxes that would result if you sell?

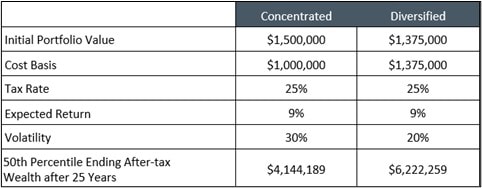

Suppose you invested $1 million in a portfolio of five stocks and held for 10 years. At the end of the 10-year period, it is worth $1.5 million for a gain of $500,000 or 50%. You are happy with the outcome and debate whether to diversify.

The cost of diversifying comes from you paying the tax bill today. Suppose your capital gains tax rate is 25%. Your tax cost in selling results in capital gains tax of $125,000. Ouch.

Yet, if you are planning on using the funds in the next few years, then sooner or later you will incur the tax. It’s a minor timing difference of when the tax is paid.

We can measure your expected after-tax wealth mathematically. Since you or no one else can predict investment returns, let’s presume both the concentrated portfolio and the diversified portfolio have the same 9% expected return. (Recall this is an overly conservative assumption in favor of the concentrated portfolio given Concentration Risks described above.)

Let’s also assume that the annual volatility of the concentrated portfolio is 50% greater than the diversified portfolio. This is consistent with how markets behave and that returns of individual stocks and of a concentrated portfolio tend to vary much more than a highly diversified one.

As seen in the table, on average you can expect to come out ahead by paying taxes and moving to a more diversified portfolio. The increase in expected after-tax wealth is larger for the diversified portfolio after just one year and becomes substantially greater over time simply because the lower-volatility, diversified portfolio is more likely to yield greater compounded returns. Paying taxes a bit sooner for a better portfolio can certainly make sense.

In part two of the article, we’ll consider not just deferring capital gains taxes but complete avoidance of them at death and also transition strategies that may further improve results of the diversified portfolio.