Roth IRA conversions – converting money from pre-tax IRAs or 401(k)s to tax-free Roth IRAs – have been a hot topic especially among high-income taxpayers since the income limitations on conversions were lifted in 2010. Converting can now be done by any taxpayer with the amount of the conversion taxed at today’s tax rate in exchange for tax-free growth and withdrawals in the future.

Basic Roth Strategy

While “tax-free” garners much attention and sounds delightful, the key variable in analyzing the efficacy of a conversion is the tax rate paid today versus the rate paid in the future. Determining today’s tax rate is relatively easily done but predicting the future, especially one determined by our Congress, is difficult at best. Yet even though you don’t know the tax rate in effect when you or your beneficiaries are to withdraw money from an IRA and pay taxes on the distribution, you still can do some sound planning.

Suppose you and your spouse are retired and make your 2013 tax projections. You see that even though you are living on $100K per year, you still will be in the 15% tax bracket. This is so because with your two personal exemptions and standard deduction, or more if you itemize, you will have roughly $20K subtracted from your gross income. Plus while some of the funds for your living expenses came from your pre-tax IRA some of the funds also came from cash in the bank and this withdrawal did not incur a taxable event.

This is a very common scenario for many retirees. In this case additional income can be realized in the 15% tax bracket – $17,851 up to $72.5K in 2013 – from a Roth conversion. Given the bottom of the bracket, it is a safe assumption that you won’t pay lower than a 15% rate in the future. Whether you pay at a 15% rate today or tomorrow is a moot point. However, if your tax rate increases in the future because of higher legislated income taxes or due to additional income through Social Security payments or IRA required minimum distributions, paying tax at a 15% rate versus 25% or more will make even greater sense.

Advanced Roth Strategy

While the Basic Roth Strategy can add value to many, for those in higher income brackets it may not be optimal. An additional layer of complexity can yield substantial benefits.

For example, suppose that you are still working and have done your tax projections for 2013 and determine that you will fall in the 33% tax bracket. With your pension, deferred compensation payments, Social Security, and other income into and throughout retirement, including required minimum distributions once you are in your 70s, it’s likely that you’ll be in this tax bracket as far as you can see. Additionally, given your financial success, you are more at risk to be subjected to increased tax rates.

Given the 33% tax bracket, you have more than $100K of room in this bracket until you reach the next higher bracket. If you were to convert $100K from your IRA to a Roth IRA, you pay tax at the 33% rate or $33K – a big check to write.

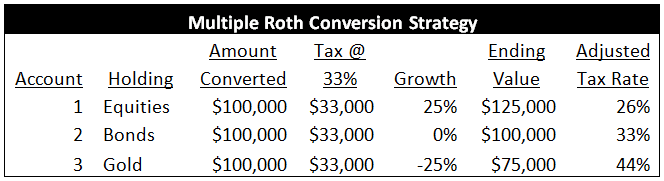

Now suppose that as part of your diversified investment allocation you want to own three distinct asset classes through mutual funds as shown in the table. It’s natural to expect that these funds will perform differently over time. This variance can be used to your advantage in order to lower your tax rate.

By converting $300K in total — $100K into three separate accounts – with the benefit of hindsight we can select the fund that performed the best and undo or “recharacterize” the other two. By selecting the best performing fund we have more in our Roth IRA but still pay tax on the $100K that was initially converted. The tax-free growth therefore adjusts our effective tax rate lower.

It is important to know that if all these funds were converted in just one account, you cannot go into the account and cherry-pick the best performer and recharacterize the rest to reap the same benefits as illustrated in the table. Thus the need for multiple accounts. Further this strategy not only generates a lot of paperwork with your account custodian but also generates a lot of tax forms for the conversions and recharacterizations. This advanced strategy adds complexity – even more than is mentioned here – but can also add tremendous value through substantially lower tax rates if you or your advisor can effectively manage it.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.