You just retired and need to start taking money from your investment accounts. After all, you have no more paycheck. You now need to create retirement income.

You open a spreadsheet to do some calculations. You figure you’ll earn a compound return of 6% over time. So, you decide to take 6% of your account value to replace your paycheck. After all, this will keep your principal intact over time.

What could go wrong? Plenty.

Bad Timing

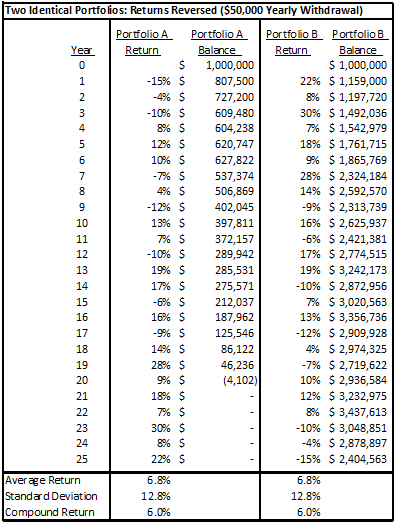

Consider this example. Two portfolios each begin with $1,000,000 and $50,000 is withdrawn yearly. Both portfolios experience the same compound returns over a 25-year period, only in reverse order. Portfolio A has bad timing with negative returns in its early years and is depleted by year 20. Portfolio B has early positive returns and ends up 25 years later with more than twice the amount of assets it started with.

Same withdrawals. Same returns – but in a different order. Dramatically different results. Welcome to what retirement researchers call ‘sequence of returns risk’ and what I call Bad Timing.

Think the Great Recession in 2008. Think the tech bubble bursting in 2000. You get the idea.

This risk, while related to investment risk, is distinctly different. After all the returns and volatility are the same.

This risk is most prevalent in the last few working years and magnified even more in the first few years of retirement. It can put you on the road to ruin. You need to plan accordingly.

Plan Stress Test

Step one is to have a well-crafted retirement plan. Your plan can then be stress tested for bad-timing risk. The results will show what, if any, of your lifestyle goals may be at risk.

Suppose your plan has five goals that you rank in order of importance to you: essential expenses or needs, healthcare, more discretionary items or wants, car purchases, and travel. Your stress test reveals that if you maintain spending on all goals, you risk running out of money. Looking further, you see that your top three goals are still well funded, which makes you feel somewhat relieved.

The bottom two goals – car purchases and travel – need some revisions. You decide that if this risk materializes you can hold onto your vehicles a couple more years, which will save some money. Considering travel, you feel traveling in your 60s is more important than later, and you are okay with the trade-off of eliminating travel expenses in your later 70s.

If bad-timing risk materializes, you now have a plan for how to act. You are not worried about running out of money or making significant spending reductions. And if returns rebound sharply after the downturn, maybe you won’t have to cut-back at all.

You’ll have to update your planning and keep an eye on things. There are also portfolio strategies to manage bad-timing risk that you’ll want to utilize when markets go south. And these are what I’ll write about next time.