Having reasonable assumptions for investment returns is critically important for many reasons. These assumptions will impact the success of your retirement plan, investment allocation decisions, and your peace of mind to name a few.

Why peace of mind? Well, if you are expecting something unreasonable, no doubt you’re likely to be dissatisfied and more likely to be undisciplined.

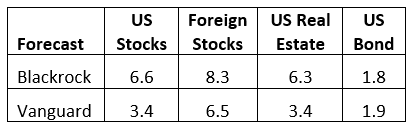

10-Year Forecasts

Blackrock and Vanguard are two of the largest global investment companies. Forecasts from them for 10-year broad asset class returns as of March 31, 2021 are provided in the table. Returns are reflected in an annualized percentage.

Upon first glance, how do these numbers strike you? Higher or lower than you’d expect?

What about the comparisons between the two? Notice how bond forecasts are nearly identical but more dispersion exists particularly for US Stocks and Real Estate? And who is right – Blackrock or Vanguard?

Building Blocks

Returns for both bonds and equities can be decomposed into various components that contribute to the total return of each asset class. Recall the total return is income return (yield) plus or minus price return (growth).

For bonds, forecasts prove to be more straight forward. The yield for a US ten-year note is about 1.6% in June 2021. The starting yields are highly predictive of prospective bond returns, explaining more than 90% of the return over historical 10-year periods. Thus the congruence of bond forecasts in the table.

Investors may go beyond government bonds and into corporate or municipal bonds, which tend to have increased risk and yield relative to US Treasuries.

Stock (equity) asset class returns are much more difficult to forecast. Where starting yields are highly predictive of bond returns, starting prices (valuation) of equities historically have shown to explain about 60% of the return variation over a ten-year period.

Equity returns can be decomposed into three key components: dividend yield, growth, and change in valuation.

The dividend yield is the income return from equities. It is easily determined and is about 1.4% today. It also tends to have little variation.

Growth and valuation are two components that have much more variability through time and also vary in the forecasts of Blackrock and Vanguard.

Valuation is the most speculative component. If you can predict how pessimistic or optimistic investors will be in the future, you can home in on this. Alas this mind-reading is impossible.

Yet, from various measurements – price to sales, price to earnings, price to cash flow, etc. – we can see that US stocks look to be priced quite expensively compared to levels the market has historically traded. In fact, both Blackrock and Vanguard believe the same and assume that valuations reserve course over the next decade and subtract 1-3% yearly. A similar decade of negative valuation change occurred in the 2000s for US stocks following the Technology Bubble in the 1990s.

Forecasting growth is also quite difficult with much variation through time. Here Blackrock is more optimistic than Vanguard, particularly for the US. The growth building block also comprises an inflation assumption. Despite recent spikes in prices, both see inflation being modest at 2 – 2.5% yearly over the ten-year period.

What Should You Do?

First and always be rational and disciplined. Higher growth stocks are much more expensive than lower-growth, value stocks. Both Blackrock and Vanguard expect that favoring value stocks – both domestically and abroad – is likely to help bolster returns over the coming years.

Additionally, forecasts favor foreign stocks over the US, so owning more of them may make sense. It’s not that expectations are for Europe or Japan to grow markedly faster than the US. Rather, the starting prices of these markets is much more favorable.

While the above comprises complex work into providing these estimates, they are just that. The world is an uncertain place.

Most importantly update your financial planning on a regular basis. Your investments need to be well aligned to your financial planning and stress tested to minimize undesirable changes to your lifestyle.