While you have enjoyed tame inflation, increasing economic growth, and higher stock prices beefing up your investments over the last 10+ years, you should never solely rely on any economic regime to dominate your portfolio or forsake diversification. Instead, the foundation of good long-term investing must be built on evidence and diversification that incorporates many different market environment environments. So how is this done?

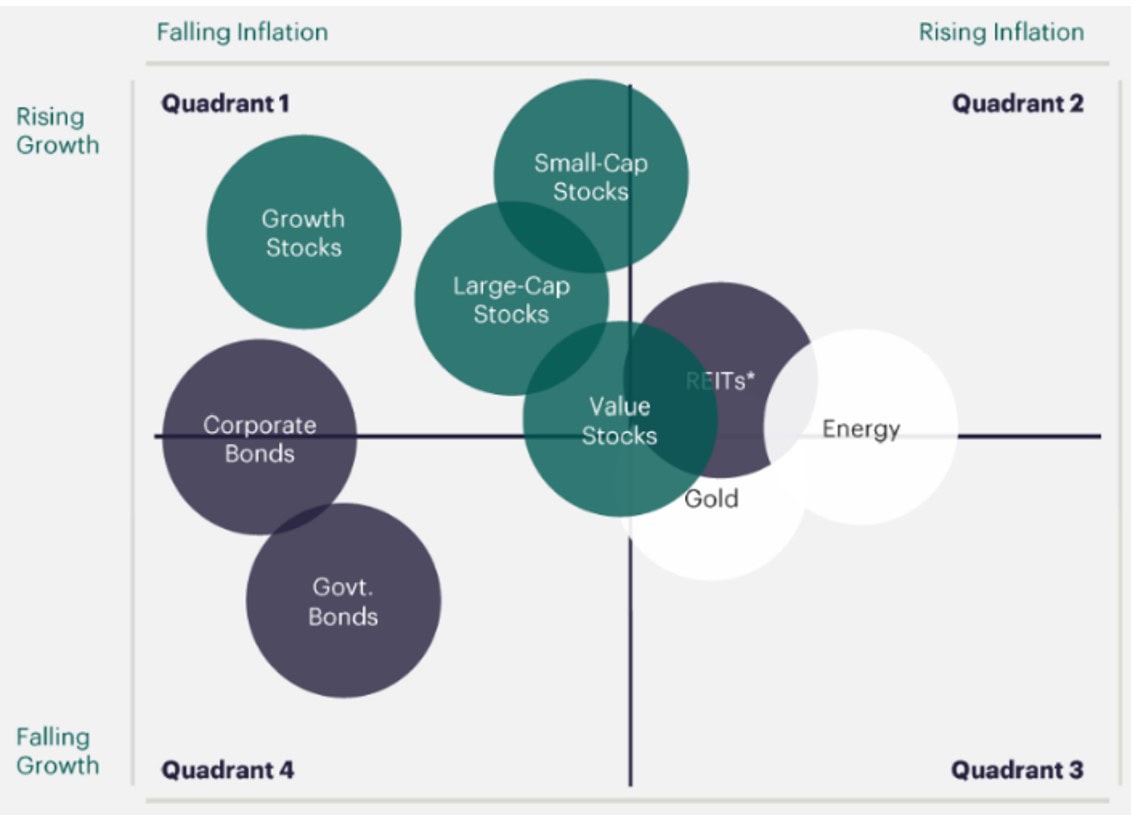

The chart shows which certain assets that tend to do better in four different economic regimes: rising growth with falling inflation, falling growth with falling inflation, rising growth with rising inflation, and rising inflation with falling growth. Famed investor Ray Dalio of Bridgewater created this framework and the associated Bridgewater All-Weather Strategy in the 1990s.

Upon first glance, you can see that many assets do well in falling or tame inflation, particularly coupled with rising growth (Quadrant 1). This regime has been dominant over the last decade. Growth stocks soared, bonds continued their 40-year bull market, and a traditional 60% stock and 40% bond portfolio has delivered the best risk-adjusted returns in the past 60 years. No doubt, most of your investment assets fall in this quadrant.

Upon first glance, you can see that many assets do well in falling or tame inflation, particularly coupled with rising growth (Quadrant 1). This regime has been dominant over the last decade. Growth stocks soared, bonds continued their 40-year bull market, and a traditional 60% stock and 40% bond portfolio has delivered the best risk-adjusted returns in the past 60 years. No doubt, most of your investment assets fall in this quadrant.

Yet, as inflation expectations increased markedly over the last several months, these high-flying growth stocks and longer duration bonds are the very same that have been taken to the woodshed in 2022. As of the time of this writing, in early May 2022, the Nasdaq is down more than -22%, and the Ark Innovation ETF (ticker ARKK) – the poster child for this high growth, low-interest rate, exuberant period – is down more than -50% YTD. U.S. Aggregate Bonds are also down more than -10% YTD.

In fact, ARKK was down more than -70% from its high in February 2021. Sadly, the preceding few months had record inflows into ARKK as the fund swelled in size. Thus, most investors didn’t experience the ride up but have fully felt the severe losses on the way down. Bad investor behavior again exemplified.

Looking at the chart, very little does well in rising inflationary environments. While energy stocks, real estate (REITs), and gold are listed and are likely to do better than quadrant 1 assets, their performance has been mixed over differing inflationary environments. Value stocks – generally slower growth, cheaper, and more cashflow generating than their growth stock counterparts – are the only asset class that generally performs reasonably well under all four economic regimes.

Not listed in the chart, trend-following strategies tend to do well in trending markets and may profit in all four quadrants. Trend strategies use assets such as stocks, bonds, commodities, currencies but may go long or short if a strong positive or negative trend exists. Trend following is a strategy not typically utilized by most investors but has long-dated evidence showing its diversification value to traditional stocks and bonds, particularly in rising inflationary environments.

Making predictions, especially about the future, as the saying goes, is difficult. Predicting economic regimes or inflation is no different. The Federal Reserve quickly changed its tune on inflation being modest and transitory to something larger and more lasting.

Rather than predict, prepare by being diversified across economic regimes. You may not have bragging rights when as growth stocks are flying, but investing science shows you will likely have higher compounded returns and more dollars over time.

Kevin Kroskey, CFP®, MBA | Managing Partner May 2022

See Also:

Inflation & Your Portfolio Part 1 – True Wealth Design (April 2022)

Why Big Tech Stocks Must Underperform – True Wealth Design (May 2020)

Should You Have Managed Futures (Trend Following) In Your Portfolio? – True Wealth Design (May 2015)