Rebalancing is the process of buying and selling investments in a portfolio to adjust their weightings back to the targeted allocation of the portfolio. It is intended to keep portfolios ‘on target’ for both their allocations and risk levels while becoming a systematic process of “buying low and selling high” to enhance returns. While this sounds easy in theory, emotional considerations often make it difficult, and the implementation process quickly gets complicated for a real-life portfolio.

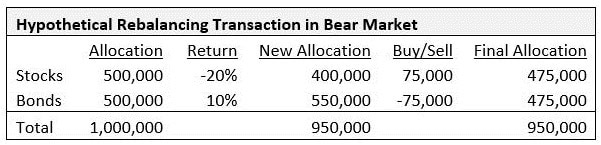

The table below shows an example of a simplified 50/50 stock/bond portfolio. After a stock market decline of 20%, the portfolio’s allocation has gone from 50/50 to 42/58 stock/bond. The goal of rebalancing would be to sell the now over-weighted bonds and buy the now under-weighted stocks. Thus, the investor would sell $75K of bonds and use the proceeds to buy $75K in stocks. The result: the portfolio is back to being 50/50 in stocks and bonds.

The rationality of buying low and selling high is self-evident. Yet, consider the emotional difficulty: you just lost $100K in stocks, which causes you pain. Will you robotically set emotion aside and follow a disciplined process, selling bonds that appreciated in value to buy more stocks that just sank? Were you able to do so in 2008? If the process is automated, it is more likely the answer to those questions will be ‘yes.’ Therefore, the question becomes how to best automate the process in the context of a real-life, multi-asset-class portfolio.

Use relative ranges rather than a calendar approach. A 2007 study by Gobind Daryanani, Ph.D., called “Opportunistic Rebalancing,” found rebalancing on a regular time-horizon such as quarterly or annually is suboptimal and missed opportunities that daily market volatility presents to enhance returns. Rather, he found using a range relative to the targeted weighting of the position was optimal.

For example, suppose U.S. Small Cap stocks are targeted at 10% of the portfolio, so the acceptable range with a 20% variance is 8% to 12%. If the position goes below (above) this range, you would rebalance to buy (sell). Daryanani found that due to market volatility, checking daily for rebalancing opportunities is ideal even if no rebalancing trade is required. He found doing so yields approximately a 0.50% increase in annualized return, which would equate to $5K yearly on a $1M portfolio.

Set different ranges based on volatility. A 2015 study by Antti Ilmanen, Ph.D. found that the more volatile an asset class is the wider the rebalancing range should be. The reasoning is that prices tend to exhibit momentum for some time – e.g. winners keep on winning. Thus if the range is too small, more frequent rebalancing trades will be made not capturing momentum effects and increasing transaction costs. This negative, small-range effect is more pronounced on asset classes that bounce around more. For example, a wider range should apply to emerging market stocks or managed futures funds that tend be more much more volatile than bonds or even U.S. Large Cap stocks.

While self-directed investors may find the strategies above to be too onerous to implement both from an emotional standpoint and from technical perspective, an astute professional advisor can automate these strategies on a daily basis with rebalancing software to more effectively manage risk with the expectation of enhancing returns over time. In a world where expected returns are historically low for many asset classes, every little bit of return enhancement helps.

See also: The Rebalancing Bonus: Theory & Practice; William J. Berstein

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.