Many investors view dividend payouts as a reliable source of income. However, many have been surprised to see lower-than-expected dividend payouts following the onset of the coronavirus pandemic. Yet, historical data show that changes in dividend policy are common, especially during times of higher uncertainty. Rather than aiming for dividends alone, focusing on income and growth, called total return, is likely to yield an improved investment portfolio and more reliable income.

2020 Changes

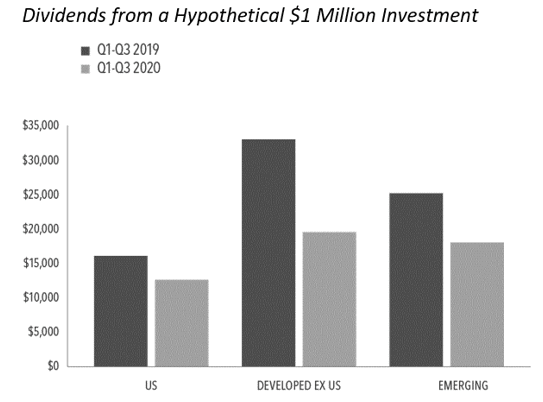

Aggregate dividend payouts fell meaningfully in the first three quarters of 2020 compared to the same period in 2019. The exhibit shows the dividends earned from a hypothetical $1 million investment in US, developed markets outside the US, and emerging markets in both periods. Developed ex-US markets showed the most drastic change with a 41% decrease. Dividend payments in emerging markets decreased by 29% and in US markets by 22%.

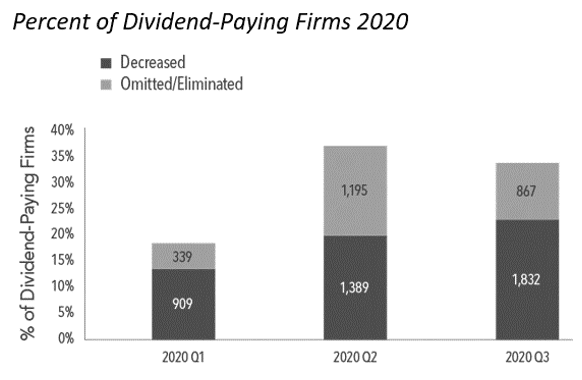

Large firms have historically had the highest propensity to offer dividend payouts, but even successful, established firms were not immune to the economic consequences of a global pandemic. For instance, Harley Davidson (HOG) has been paying dividends to shareholders since the 1990s. In April 2020, the motorcycle manufacturer slashed its dividend from $0.38 per share to just $0.02, a 95% decrease. Gap Inc. (GPS) suspended its dividend payments until at least April 2021 after the economic downturn left the clothing brand with particularly poor revenues. Even General Electric, a company that paid dividends consistently for a century, slashed its payout to just $.01 per share, and this was before COVID.

While these dividend cuts may come as a surprise to some investors, the Great Recession had a similar occurrence. In 2008, the global market was down more than 40%, and, the following year, many firms made changes to their dividend policies. In 2009, Harley Davidson, for example, announced it was cutting dividend payouts from $0.33 per share to $0.10, a 70% decrease.

Total Return

While dividends are not bad, it is better to focus on total return, which accounts for growth (or loss) alongside income. The benefits of doing so include improved diversification, more flexibility, and greater tax-efficiency. If income needs derived, simply sell a portion of your portfolio to raise cash and create your dividend.

In terms of diversification, the average proportion of firms paying dividends in the US was about 52% from 1963 through 2019, meaning an investor focusing only on dividend stocks is missing out on nearly half of investible US companies. Ignoring half of the investment market does not make sense.

That number has declined after 1982 when an SEC rule was changed and allowed companies to repurchase their outstanding shares. These buybacks are more tax-efficient than dividends and have become the preferred method of many corporations to return money to their shareholders. Dividend yields have thus been declining for decades: For the S&P 500, they were as high as an average 9.2% in 1938, but only average 1.6% today.

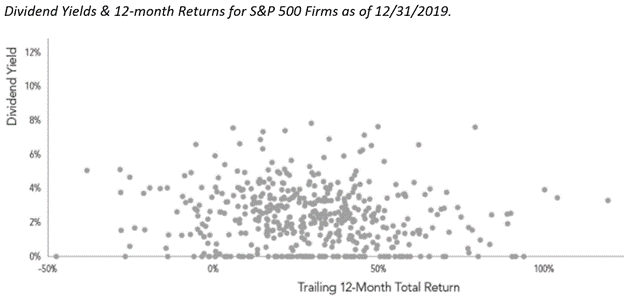

It is essential to point out that despite common beliefs, high dividend yields may not lead to high total returns. The exhibit below plots the trailing 12-month returns of S&P 500 Index constituents as of December 31, 2019, with each dot representing a company. It’s clear that companies with greater dividend yields, the dots located higher up the vertical axis, weren’t consistently those with a higher total return over that period.

Summary

The first three quarters of 2020 remind us that dividend payouts can be inconsistent, particularly in volatile markets. Hence, investment strategies that focus on income derived from dividends may not serve investors who need a steady income stream and might not be the most effective way to pursue long-term wealth growth. A more reliable approach is to structure equity asset allocation around the characteristics that research demonstrates drive long-term higher expected returns, namely size, relative price, and profitability, while maintaining broad diversification across names, sectors, and countries.

This article written by Kevin Kroskey, adapted with permission from Dimensional Fund Advisors.

See Also:

The Science of Investing & Factors You Can Use To Build Better Portfolios – True Wealth Design

Why Your Retirement Income Strategy Needs to be Dynamic – True Wealth Design

Ep 16: Retirement Income Planning Series – Part 1 – True Wealth Design

Ep 17: Bad-Timing Risk: Retirement Income Planning Series – Part 2 – True Wealth Design

Ep 18: Total Return Portfolio: Retirement Income Planning Series – Part 3 – True Wealth Design

Ep 19: Dynamic Strategy: Retirement Income Planning Series – Part 4 – True Wealth Design