Investors often use haphazard methods of selecting investments and completely ignore the science of investing. For decades now, academics have studied investment markets and conducted empirical research to try to identify what works and what does not work when it comes to investing. Over time, these studies have yielded various “factors” that work and quantify risk and return. These factors can be taken from the classroom and used to build better portfolios.

Science and Statistics

Finance is not a hard science like Physics where there are immutable laws. Rather, finance is a social science and the scientific process generally requires drawing inferences from “noisy” historical data. This noise often leads to confusion and erroneous conclusions. However, statistics can help investors have a much better frame of reference for interpreting results that help us hone in on our best guess.

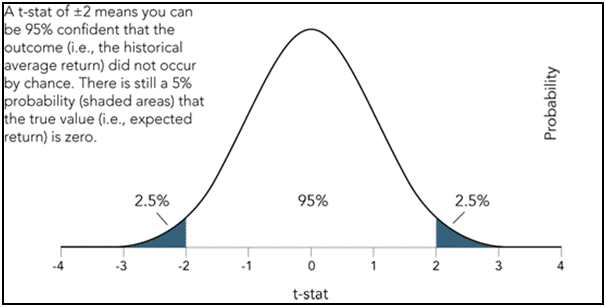

When formulating forward-looking return estimates, it makes sense to first start using historical averages. We can separate the historical noise from true underlying factors by using the bell curve that you thought you’d never use again after leaving high school. I’ll spare you the technical discussion. Just know that the generally-accepted approach uses a 95% confidence level to identify a true factor, and the 95% confidence level corresponds to a t-stat of 2.0. The higher the t-stat and confidence level, the more reliable are the data.

Investment Factors

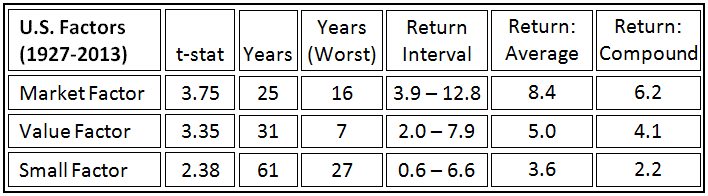

We’ll focus on the three main and most well understood factors. The “market factor” is the excess return from taking equity market risk versus leaving money in treasury bills. The “value factor” is the excess return from owning out-of-favor stocks with lower prices rather than higher-priced, less-risky growth stocks. The “size factor” is the excess return from owning small stocks compared to larger, better-known stocks. It is important to note that excess return is just that. These factors have abnormally higher returns than what generally-accepted investment models predict. So you can in effect expect more bang for your risk buck.

To explain the table, the factors are all considered statistically significant with t-stats above 2. The years column is the number of years required, statistically speaking, to have at least a 95% confidence that the factor will yield benefits. The Years (Worst) column outlines the longest actual historical period without a positive return from the factor.

Most are surprised at how long of a time period it takes to reliably separate the noise and truly identify a factor. This is a daunting proposition, considering that most investors equate long-term more likely in the range of three to five years. Few inferences can ever be drawn from short periods of time.

The confidence interval quantifies the actual range of return that can be expected for the risk factor and the average return is just that. It is important to note that due to investment volatility compounded returns, which are what investors receive, are always lower than average returns.

In practice these factors on a forward-looking basis are likely lower than what we have observed in the past. Yet, they are still likely to persist and can be utilized to build better portfolios and earn excess returns. These factors not only apply to the U.S. market but global investment markets.

Conclusion

I realize this article may have been a tough read even though I tried to spare the technical details. Yet, we have only scratched the surface. Einstein said, “Everything should be made as simple as possible, but not simpler.”

Prudent investing is a scientific and mathematical process. It is not picking a stock because you like the dividend yield, buying the S&P 500 because it has done well, or selling your investments and going to cash because you were influenced by a negative news story. These methods are haphazard at best but often quite hazardous to your financial health and certainly no way to invest your life savings.

Understanding the science of investing is a much more reliable method to build a prudent portfolio and earn the returns you need to make your financial life plan work. Great discipline is still required.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.