As broad market indices such as the S&P 500 have set new record highs in 2014 and then recently became more volatile and retreated, many investors have become apprehensive. They fear another major decline is likely to occur and are eager to find strategies that promise to avoid the pain of an extended downturn but preserving the opportunity to profit in up markets. One approach that has attracted considerable attention in recent years is adjusting investments based on the CAPE ratio–the Cyclically Adjusted Price / Earnings ratio.

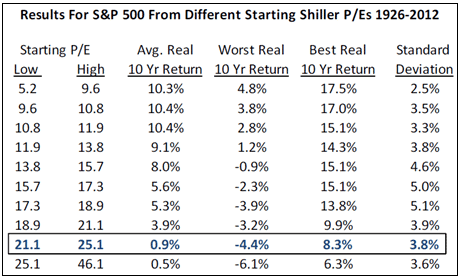

Developed by Robert Shiller of Yale University, the CAPE ratio seeks to provide a road map of stock market valuation by comparing current prices to average inflation-adjusted earnings over the previous 10 years. The idea is to smooth out the peaks and valleys of the business cycle and arrive at a more stable measure of corporate earning power. Advocates suggest that investors can improve their portfolio performance relative to a static equity allocation by overweighting stocks during periods of low valuation and underweighting stocks during periods of high valuation.

A CAPE-based strategy has the virtue of using clearly defined quantitative measures rather than vague assessments of investor exuberance or despair. Using the CAPE ratio might appear to offer a sensible way to improve portfolio results by periodically adjusting equity exposure. Does it work?

The challenge of profiting from CAPE measures or any other quantitative indicator is to come up with a trading rule to identify the correct time to underweight or overweight stocks. It is not enough to know that stocks are above or below their long-run average valuation. How far above average should the indicator be before investors should reduce equity exposure? And at what point will stocks be sufficiently attractive for repurchase–below average? Average? Slightly above average? It may be easy to find rules that have worked in the past, but much more difficult to achieve success following the same rule in the future. The performance record of professional money managers over the past 50 years offers compelling evidence that market-timing efforts have failed.

You will never know the path the returns may take on a day-to-day or even a year-to-year basis. However, using CAPE in conjunction with other valuation metrics over longer periods does seem to have some predictive power. Most importantly, these can be used to help formulate realistic expected return assumptions for your retirement plan. The CAPE around 24-25 today implies forward looking returns over the next several years do not look rosy and certainly less than historical returns. The same is true for fixed income returns. Yet fixed income is not exposed to the downside risks that equities are.

Short-term timing does not work and is akin to a coin-flip. Going out in time over a full business cycle, expected returns have some predictive power using good inputs and analysis to forecast them. Now is a great time to update your retirement plan and ensure you are using reasonable expected returns and ensure your investment portfolio is prudently positioned to meet your retirement cash flows.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.