A recently publicized Akron-area Ponzi scheme took in nearly $21 million from 47 people, SEC lawsuit says. A fake company was established that was marketed to investors as a business that buys and sells oil and refined fuel products. Investors were told they could earn 2 percent to 4 percent monthly, or 24 percent to 48 percent a year, with no market risk by buying promissory notes in the company, according to the court charges.

This sort of fraud is inexcusable but so is the greed and ignorance of the investor in this type of scheme. In a world where banks are paying yields below 1% on cash deposits, why would someone pay 24% to 48% per year?

Risk and return are related. As investors we are compensated for market risk we take. Other risks are not compensated like single stock risk, aka ‘security selection risk.’

Risk and return are related. As investors we are compensated for market risk we take. Other risks are not compensated like single stock risk, aka ‘security selection risk.’

The only free lunch in investing is diversification. If you are looking for a silver bullet, you are more likely to end up ruined from one than rich from one. Promissory notes or other ‘private investments’ are often the bullet that kills you. While they can be legitimate, they are opaque and are laden with abuse by fraudsters. Why accept the lack of transparency and take this non-compensated risk?

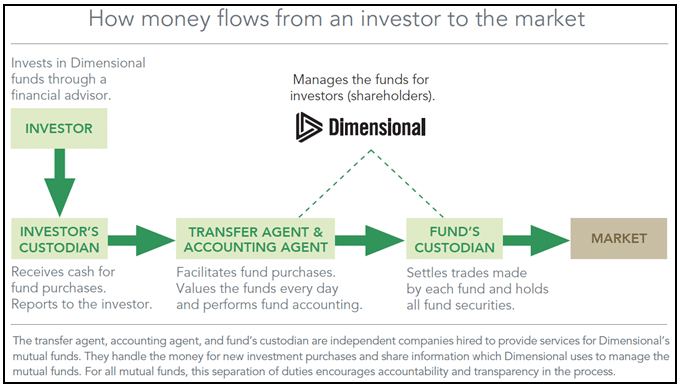

When something like this occurs, it is good to revisit how mutual funds are transparent and consumer friendly. A diagram of how money flows in a mutual fund is provided from Dimensional Fund Advisors, an institutional mutual fund company. Mutual funds:

- Are regulated under the Investment Company Act of 1940, which requires extensive disclosure of material details about the funds.

- Provide a prospectus and annual reports, detailing results, fees, expenses, and objectives.

- Publish financial statements that have been independently audited and updated regularly.

- Provide 1099s rather than K-1s as private investments do, which makes tax preparation more difficult.

- Are required to maintain a board of directors, a majority of which are independent from the fund company itself.

- Utilize a qualified custodian who takes possession of the securities purchased. The qualified custodian is generally a bank that is required to segregate mutual fund securities from other bank assets. This separation between fund management and custody is mandated by law and serves investors since the mutual fund is trading securities on their behalf as shareholders.

- Open-end mutual funds provide daily liquidity at net asset value. Private investments often have limited liquidity and long-term lock-up features.

- In the event a mutual fund company ceases to do business, the securities would remain with the custodian while the mutual fund’s board of directors would decide whether to hire another fund manager or sell the securities and distribute the proceeds to shareholders.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.