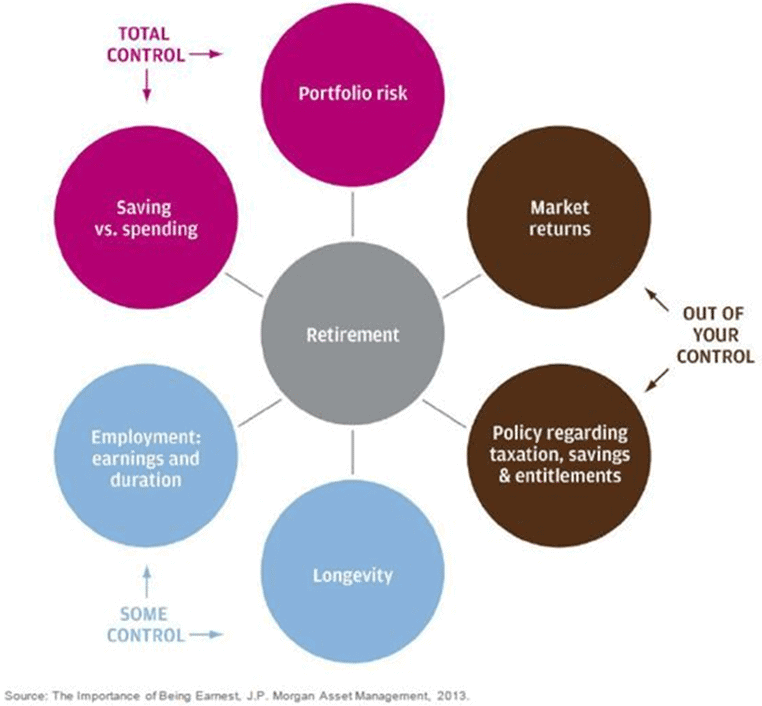

When are you going to retire? How much are you going to spend in retirement? These questions increasingly have become more complicated.

A diminishing number of people actually plan to leave work and embrace leisure on a full-time basis. Many surveys show that pre-retirees expect to work beyond age 65. However, even though they expect to work longer, they do not in practice.

A 2013 Employee Benefit Research Institute (EBRI) study showed that 68% of employed Americans planned to work beyond age 65 but only 25% of current retirees actually did. A number of factors caused people to retire earlier than expected, including health problems, employer issues, and family obligations. On a positive note, others retired sooner because they were able to do so financially earlier than expected.

When people do retire, assumptions about their spending habits will have to be revisited. It was assumed that in the vigorous early years of retirement, people would spend in addition to their regular lifestyle expenses more on travel and other leisure activities than they did when they were working. So their overall expenses would go up the day after they retire and gradually diminish. At some point in the age curve, health expenses would start to rise. The people who study retirement expenditures talked about a “smile” graph of expenses, where it cost more to live and play in the earlier and later years of retirement than in the middle years.

What is wrong with that? For one thing, when you look at the EBRI or Bureau of Labor Statistics data on what people actually spend in their later years, it contradicts this comfortable smile pattern. Yes, you will spend more on healthcare as you age, and your housing costs will stay relatively consistent. However, a clear trend emerges to show that spending declines throughout retirement mostly from the spending categories of education, entertainment, food and beverage, and transportation and these declines are greater than the offsetting healthcare increases.

Yet when you dig even deeper and look at income variances other insights emerge. For instance, high-income retirees may continue to spend at higher levels. However, the character of their spending often changes with a larger percentage of their expenses going to more discretionary items such as donations and gifts. With the benefit of hindsight, these high-income retirees can afford to do more for others while not sacrificing their own long-term financial health.

How can we predict these things in advance? We cannot. In addition, it is important to remember that these broad statistics do not apply to your individual circumstances. They just demonstrate the averages and suggest things that most of us should watch out for. The only clear conclusion of the research, thus far, is that we should probably make conservative assumptions about spending and keep a close eye on our retirement planning as assumptions become realizations and life happens.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.