When Nobel winner Eugene Fama studied the long-term performance of U.S. equities in the early 1990s, he found that stock returns had decreased with size and cost. The smallest, cheapest companies had provided higher investment returns than the biggest, costliest firms.

Though initially counter-intuitive to many – why wouldn’t you want to invest in the biggest and best companies? – it made sense. Large-growth stocks were safer economic choices, operating reliable businesses well-positioned to survive recessions. Thus, they were handsomely valued, at prices that limited their potential for future increases.

Said another way: less risk should lead to less reward. The market’s behavior appeared to be logical.

But logic tends to prevail over time in markets and not on a monthly, yearly, or even multi-year basis. The logical relationship persisted for two decades from the 1990s through 2009, despite a few year distortion during the Tech Bubble of the late 1990s, with the Russell 2000 Small Value Index returning an annualized 10.3% versus 7.5% for the Russell 1000 Large Growth Index. Yet, that relationship has not held up more recently.

From 2014 through 2020, the large growth index outperformed the small value index by an annualized 11.2%, capped by a whopping 33.9% outperformance in 2020.

Entering 2015, the companies in the large growth index traded at an average price of 24 times their trailing earnings. Entering 2021, they carried a multiple of 45, meaning that for the same amount of earnings, large-growth investors are paying 87% more than in 2015.

Over that same period, the large growth index grew earnings by 40% while their collective stocks prices appreciated by 160%. Thus, about 25% of the gain can be attributed to improved earnings while 75% resulted from investors simply paying higher prices.

Opposite to large-growth stocks, the small value index decreased in the average price paid for earnings, falling from 16 times earnings at the start of 2015 to 15 times in 2020. Over the period, earnings grew by 31% while prices increased by only 23%.

While large-growth companies have posted higher earnings gains than small-value companies, that edge has been unexceptional. Low interest rates may help explain some of the differential but that is modest at best. Thus, the real explanation behind the great divide lies neither with earnings, or with changes in interest rates, but instead with investor expectations. Over the past several years, stock buyers have become far more optimistic – perhaps delusional in some cases – about large-growth fortunes, even as they have soured on those of small-value stocks.

Covid & Reopening

As expected, large growth stocks held up materially better through 2020 as their earnings were more resilient than small cap value counterparts. Additionally, the larger technology exposure in large growth proved fortunate. Earnings were accelerated for many of these companies as the world scrambled to make investments to work and survive through our social distanced world. This acceleration is also likely to dampen their future growth.

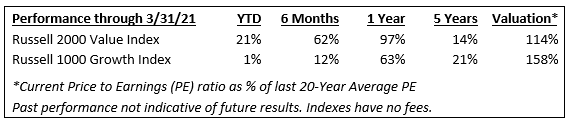

Even though small, cheap stocks were marked down in price severely in February and March 2020, the rebound has been equally astonishing. Since the Moderna phase 3 study results were first announced in November 2020, small value stocks have been on a relative tear. They are up 21% in 2021 through March and up 62% over the last two quarters – 20% and 50% more than the large growth darlings, respectively.

Despite their recent tear, these small value companies are still reasonably valued, trading at a slight premium relative to their 20-year average. Further, these companies are expected to have substantial rebound to earnings growth over the coming years as the economy reopens; more so than their large growth counterparts.

As Yogi Berra said, “It’s tough to make predications, especially about the future.” If you could have predicted how people – collectively the market – were going to feel in 2015 and subsequently behave over the coming years, you could have profited from their bidding up of prices in large growth stocks. Today, however, it seems the pendulum of logic is fiercely swinging back against this exurberance and, in my opinion, is likely to continue swinging in this direction for some time.

Kevin Kroskey, April 2021