One of the most common mistakes pre-retirees make is not matching their investment portfolio to meet the monthly cash flows needed for their retirement goals. Rather, the investment portfolio chosen arbitrarily, not linked, and often mismatched from the retirement spending goal. At worst, this can have disastrous consequences of not being able to adequately fund retirement goals, and, at best, it requires the retiree to have substantially more in savings compared to having more of a matched strategy.

A matched strategy is most simply exemplified in this manner: Let us say that you will need $100K from your portfolio in 2026 to meet your retirement goal. The safest way to reach that goal is to buy $100K face value 10-year zero coupon Treasury bond maturing in 2026. Such a bond currently has a yield of 1.625%, which means it will cost you about $85K to buy it today. There are no interest payments to you. While the value of this bond will likely fluctuate from the time of purchase until maturity, you are assured to receive the $100K upon maturity in 2026.

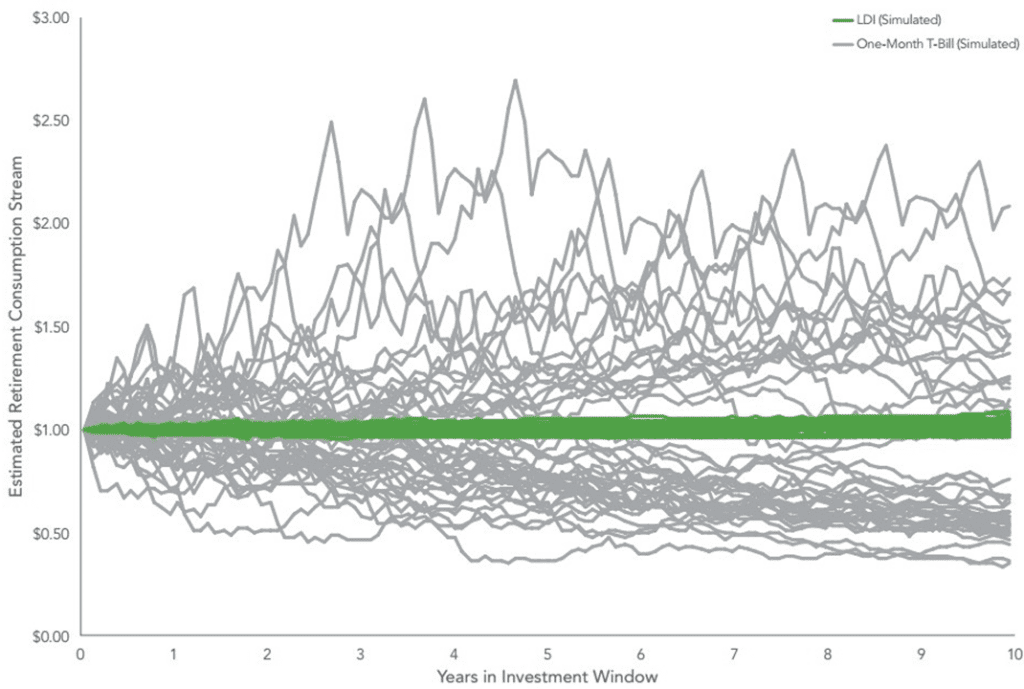

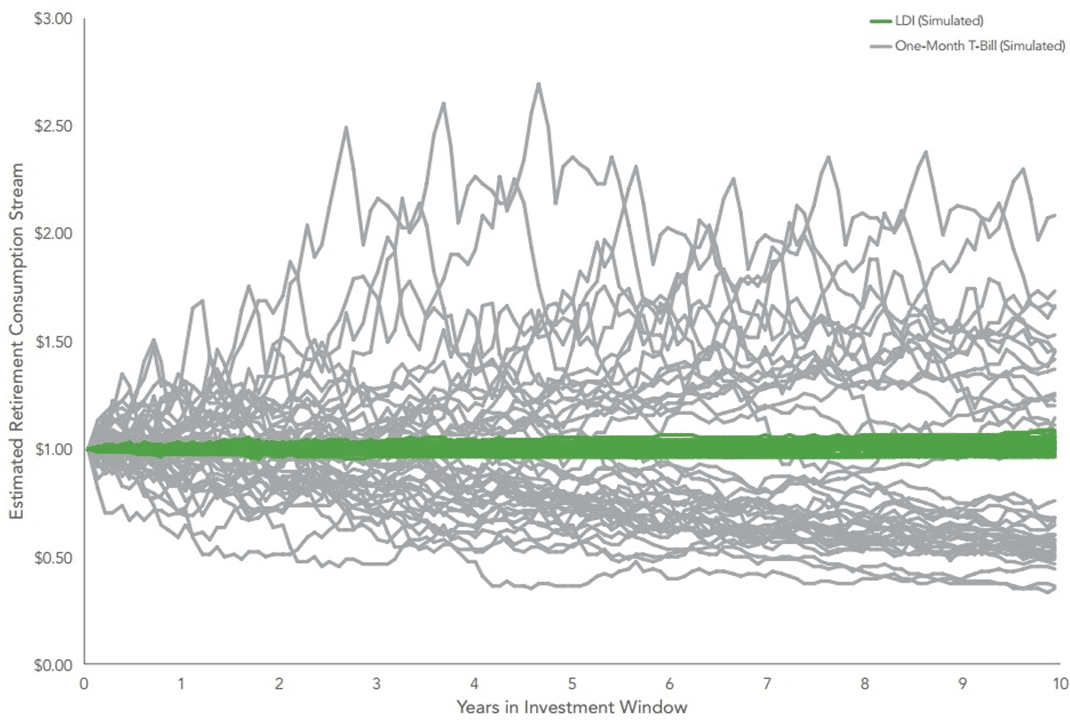

Now let us consider Tom who is planning to retire in 10 years at age 65. For simplicity, assume Tom’s retirement goal is defined as a $1 monthly check for 25 years to age 90.

Consider two investment strategies. The first strategy attempts to match each of the 25-year monthly checks. The second strategy uses a simple cash savings account, proxied by one-month US Treasury bills. The cash strategy may be perceived as comfortable, principal-protected, and low risk. However, the cash strategy is much riskier in the context of meeting future retirement expenses.

Using available interest rate data between 1962 and 2015, we construct a simulation showing how much of Tom’s $1 per month retirement goal is met by the two strategies. The pattern is clear. The matched strategy (denoted by “LDI”) is relatively stable and near his goal in all outcomes. The cash strategy is a rollercoaster, ranging from meeting about one-third of his goal to being able to spend twice his goal.

The median outcome of $0.67 for cash is well below $1 median under the matched strategy. Why? The matched strategy is a strategy that better manages retirement risks, having the same sensitivity to interest rates as the future retirement spending need. This matching also tends to use longer-term bonds that generally have a higher yield than cash.

How can Tom increase the likelihood of meeting his retirement goal if a cash-like strategy is the only option he feels comfortable with? He needs additional, precautionary savings. Generally, the less effective the risk management available, the more savings are needed. The value of an effective risk management strategy is that it reduces the need for precautionary reserves. So in effect, it is possible to retire sooner or with more confidence if a matched strategy is properly planned and implemented.

Cash matching strategies use short-term assets to meet short-term spending needs and longer-term assets to meet longer-term spending needs. Pension plans have long used cash matching strategies to effectively meet the monthly payments promised to workers for their lifetimes. Though more complicated to implement for those nearing retirement, sound retirement planning advice should use matching strategies as well.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.