In prior columns, I explained how there are two schools of thought on retirement income: one being investments or probability-based and the other being insurance-based strategies with an underlying guarantee. While guarantees sound good, they’re expensive, and I’ll show this in a future column.

I also demonstrated how ‘Bad-Timing Risk’, having a sequence of negative returns early in retirement, is one of the key hurdles in following an investment-based approach. Yet, with proper planning, this risk can be stress-tested against your spending plan to more clearly see what lifestyle goals, if any, may be at risk of being reduced. This stress test is also instructive as to how to match your investment portfolio to meet your spending goals, which is where we’ll go next.

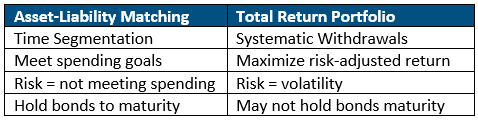

Asset & Liability Matching

Your retirement spending is a liability against the assets you have accumulated. The liability you have should be matched with appropriate assets to meet that spending. This matching is also known as a time segmentation strategy.

Pension funds have long used asset and liability matching to invest the pension fund to meet monthly pension payments. Goodyear Tire & Rubber, as an example, has a pension plan that, as of 2016, had more than $1.8 billion in assets and about the same amount in liabilities – the monthly pension payments. The plan was frozen in 2008 and is no longer accumulating liabilities but decumulating. Given this and that the plan is well funded, plans assets had an investment allocation of 94% in fixed income investments and 6% in stock investments.

Despite many of the monthly payments being decades into he future, the plan was able to meet its obligations almost solely with bonds. The plan’s objective was to meet the monthly pension payments. So, if it can do so without the risk of stocks, why do so? This is asset liability matching.

Total Return Investing

You are much different than a pension plan. Pension plans do not pay taxes and have consistent spending that doesn’t increase with inflation. You own accounts that are taxed differently, have tax rates that vary over time, and have some smooth spending but other goals that are lumpy, occurring just once or from time to time. Your spending also increases over time with inflation – a moving target. Plus, emotion enters the equation much more so for you than a pension.

Because of these and other differences, despite asset-liability matching strategies being great for deriving income in the case of pension plans, they fall short for you. A more flexible, total return investment strategy – one that seeks to maximize risk-adjusted return from a combination of stock, bonds, real estate, and other investments – needs to be incorporated.

In practice, you need to blend both of these probability-based strategies to create retirement income. Your well-crafted financial plan is stress-tested to measure how much capacity for risk you have and how much risk you need to take to achieve your required investment return. If your plan is well-funded, you may require a relatively small return for your plan to work and can invest very conservatively in fixed income investments like the Goodyear pension plan. However, you may also decide to pursue higher returns to leave more to your kids, grandkids, or charity and if the increased risk does not pan out, it likely will not hinder your lifestyle.

Conversely, you may also find that you must accept higher levels of stock risk in your portfolio to have the expectation of achieving your return objective and meeting your lifestyle goals. Yet, if you invest too aggressively, you may find that bad-timing risk causes your plan to fail and you have to reduce spending.

Your capacity for risk is related more to asset-liability matching and your required return is more related to a total return strategy. Both of these strategies are important in deriving your retirement income. Next time I’ll discuss what this means in terms of your investment allocation in more depth and how this allocation – or mix of stocks and bonds – generally should change over time … but probably not how you think.