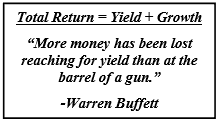

It is common that someone approaching retirement starts focusing on principal preservation. In fact, it often seems that retirees swear allegiance to a commandment: “Thou shall not invade thy principal.” This mindset causes a focus on income-oriented investments rather than focusing on the total return – income plus growth – that can be expected from a portfolio. For a multitude of reasons, this income focus is shortsighted and inefficient.

The traditional appeal of yield stems from often unconscious behavioral and economic biases. Investors prefer yield because it is easily noticeable and believed to be more reliable whereas growth is more ambiguous and uncertain. For stocks, there is the economic belief that stocks paying high dividends are less risky because they offer a  regular stream of payments to investors. However, dividend payments are not created out of thin air nor guaranteed. They flow from a company’s earnings, which are impacted by economic forces and are reflected in the current stock price. Many companies, for instance, had to reduce or eliminate dividend payments through the economic shocks of 2008.

regular stream of payments to investors. However, dividend payments are not created out of thin air nor guaranteed. They flow from a company’s earnings, which are impacted by economic forces and are reflected in the current stock price. Many companies, for instance, had to reduce or eliminate dividend payments through the economic shocks of 2008.

regular stream of payments to investors. However, dividend payments are not created out of thin air nor guaranteed. They flow from a company’s earnings, which are impacted by economic forces and are reflected in the current stock price. Many companies, for instance, had to reduce or eliminate dividend payments through the economic shocks of 2008.If a company has accumulated excess cash after reinvesting for its operations and setting aside for reserves, it essentially has two options. One, pay the cash to its shareholders as a dividend, or two repurchase its shares. No matter which option the company chooses, its investors fare the same, ignoring taxes.

For example, suppose that a company paid out 5% of its share price as a dividend. A shareholder who has $100 worth of stock would now have $95 of stock and $5 of cash. Now suppose that the company instead decided to repurchase 5% of its outstanding shares. If our $100 shareholder were to sell 5% of his shares, he would again be left with $95 of stock and $5 of cash.

Holding a portfolio that emphasizes dividend-paying stocks may force significant tradeoffs related to diversification and expected returns. For example, a global dividend-focused portfolio would exclude 35%–40% of stocks that pay no dividends, resulting in lower diversification. In addition, the number of U.S. and international firms that pay dividends is shrinking—from 71% of the market in 1991 to 61% in 2012.

Holding only dividend-paying stocks may also affect investors’ ability to pursue higher expected returns. Global portfolios holding only dividend-paying stocks exclude about 47% of the available small cap stock universe, which historically has offered higher expected returns than large cap stocks.

As for fixed income, reaching for yield involves either going into longer maturities or into lower credit quality instruments. Longer maturities will suffer the most in a rising interest rate environment and lower credit quality investments become more equity like than bond like especially in times of market stress.

Finally, as it relates to meeting retirement cash flows, living solely off yield is restrictive and nearly impossible today without markedly increasing the risk on your portfolio. Yields on higher-quality bonds are in the 1-3% range and the yield on the S&P 500 is less than 2%. Assuming a $1M portfolio, you can produce roughly $20K in income from these, and this income level fluctuates over time. Do you want to reduce your lifestyle because the yield on your investments has gone down? Alternatively, would you rather have a total return approach, a more optimal portfolio, and more consistent spending throughout retirement?

Focusing on income-oriented investments can result in these and other unintended consequences in a portfolio. For a retiree using a total return approach, once the retirement plan cash flows have been clearly identified and the overall allocation decision has been made to match these cash flows while considering total portfolio risk and expected return, the income produced becomes a byproduct. Normal pruning to the portfolio can then raise cash flows to meet retirement needs with great flexibility and simultaneous rebalance the portfolio to the desired allocation.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.