Big money can be made from hedge funds. If you run one, that is. That’s the conclusion of a new book that says people who invest in hedge funds would have been better off over the past nine years if they had stuck to a broadly diversified portfolio of vanilla stocks and bonds.

The book is The Hedge Fund Mirage: The Illusion of Big Money and Why It’s Too Good to be True, by Simon Lack, an asset manager who formerly chose hedge funds for major US bank JPMorgan. Lack argues that the 18% cumulative return on hedge funds in the nine years to November 2011 was easily beaten by the cumulative 29% gain from the S&P 500 index. The gap was even starker for investment grade corporate bonds, which in the same period gained 77%, as measured by the Dow Jones Corporate bond index.

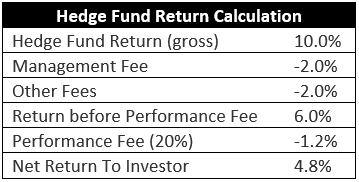

Of course, the underperformance of hedge funds over this period is even greater once the customary 2% management fee and 20% performance fees charged by hedge fund managers are taken into account. Other fees are often tacked on for accounting services, trader bonuses, and operating expenses. A study by LJH Global Investments, an advisor to hedge fund investors, found that for about one hundred hedge funds the average bill for “other expenses” was 1.95%.

Interesting to note that the hedge fund manager receives the 2% management fee regardless of whether the fund performs well. Further, the fund receives 20% of the positive performance, yet doesn’t participate in any downside. The investor, however, participates fully in any downside. This asymmetric characteristic is great for the hedge fund manager but highly undesirable for the investor.

Hedge funds often have a ‘high watermark’. The fund cannot collect any performance fees unless it first passes the high watermark and makes up any prior negative performance. To reach the high watermark, the fund manager may be tempted to take on greater risk, which could be undesirable to the investor. The fund manager may also simply shut down the fund, returning assets to investors, and start a new fund. In this case the high watermark never comes into play.

If individual hedge fund managers are generating the desired “alpha,” or additional returns above a representative benchmark, then the benefits of that skill tend to go to the managers themselves rather than to investors. In fact, Lack estimates that from 1998 to 2010, the hedge fund industry captured at least 86% of the returns it earned for its customers. This might explain why yachts cruising the Caribbean tend to be skippered by hedge fund managers, not investors.

For anyone who has followed the hype surrounding hedge funds for many years, this is not really a surprise. A good proportion of the investing public—egged on by the financial media—genuinely wants to believe that consistent market-beating returns are achievable without taking on additional risk and paying excessive fees. Yet there is no such silver bullet.

From a marketing perspective at least the appeal is fairly evident. After all, the more exclusive you make a club, the more likely people will pay a premium for joining it. Yet when analyzing the returns mathematically, it is evident that exclusivity doesn’t translate into wealth creation for investors.

While the hedge fund industry no doubt would contest the findings of Lack’s book, one doesn’t have to agree with his numbers to still harbor reasonable doubts about risking one’s hard-earned savings by investing in hedge funds. In a recent white paper, Dimensional Fund Advisor’s senior associate in Research Ronnie Shah explains that, due to the lack of disclosure around returns, it is difficult to determine how much alpha, if any, hedge funds generate.

Industry groups that report hedge fund returns rely on voluntary disclosures by the funds themselves on the returns they generate. Shah notes this creates potential for biases in the data, such as the omission of poor returns or the dropping out of the returns of failed or discontinued funds. This is in addition to other drawbacks of hedge funds, such as illiquidity, relative lack of oversight, the additional costs of leverage and derivatives and, of course, the substantial fees charged by the managers themselves.

Shah’s paper concludes that the highly uncertain payoff from hedge funds, the high expense ratios, and the lack of disclosure around them mean that investors should exercise caution before investing in them. David Swenson who manages the Yale Endowment notes when comparing investing in hedge funds to mutual funds, “Investors in hedge funds face dramatically higher levels of prospective failure, due to the materially higher levels of fees.” Probably best to forego joining the exclusive club and opt for a lower cost, transparent, and tax efficient portfolio. Doing so would make you eligible for the club of smarter investing.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.