Cognitive impairment throughout retirement and into old age is not a misfortune that strikes some but leaves others unscathed. Increasing evidence shows cognitive decline is natural, inevitable, and not slowed by education or solving crossword puzzles. Like the rest of our bodies, our brains lose their ability to quickly and accurately respond over time. How can we plan for this?

Awareness

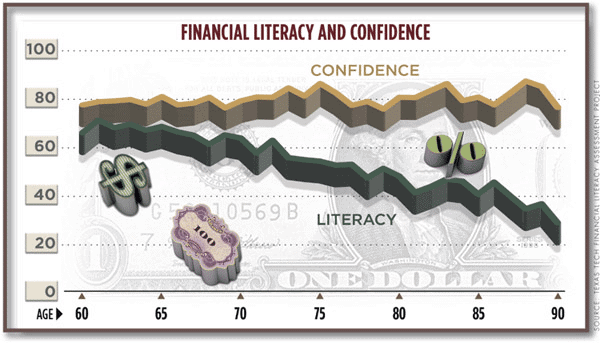

Several academic studies on credit and investing decisions and overall financial literacy show that financial decision-making abilities peak sometime in the mid to late 50s. Overtime, ability will slowly but consistently decline. Yet, this decline is not the core issue.

Dr. Michael Finke of Texas Tech wrote, “While financial abilities decline with advanced age, confidence in one’s ability to make financial decisions does not. In fact, respondents in their 80s believe their financial knowledge is slightly higher than do respondents in their 60s. This inability to assess a decline in skills with age is not limited to financial decisions. Other study results find that subjects over age 65 do not perceive their decline in driving ability despite clear evidence of reduced visual acuity and reaction times. In fact, older drivers who had multiple crashes were no more likely to rate their driving ability as worse than average.”

While decline is a concern lack of awareness of the decline is a bigger concern. This helps explain why sweepstakes frauds, Nigerian investment schemes, and other scams target seniors and retirees.

Planning for Decline

What can you do to protect yourself from bad financial decisions? Documents such as a durable power of attorney, medical power of attorney, will, trust, and advanced medical directives should be implemented well before any capacity concerns arise.

You can also simply your financial life by consolidating checking accounts at one bank and the investments at a single financial advisor or custodian. If there are many credit cards, just leave two: one for daily purchases and one for automatic bill payments. Sign up for text or email alerts from your financial institutions to notify you of unusual account activity.

Working with a trustworthy and competent financial advisor – someone who you identified and began working with well in advance of any decline and who will not retire soon after you do – can also help. Have signed documentation that the advisor can contact your power of attorney to discuss financial matters when diminished mental capacity is observed. At advancing ages, bringing a trusted child into meetings with your advisor may also be a good idea.

For childless retirees or those who may not have a trusted younger guardian to help, planning earlier in retirement for diminished mental capacity becomes even more important. Consider moving a continuing care retirement community where you can live independently but have access to more skilled healthcare within the same community, if the need arises. If you prefer to stay in your home, consider an independent care manager (www.aginglifecare.org) that can help coordinate and oversee home healthcare and other services. Bill pay services from a CPA or similar firm can help ensure day-to-day financial management tasks are being taken care of properly.

There will likely come a point when managing financial matters becomes too complex and overwhelming. The best advice here is have a plan in place. When you are your more competent and less confident self, write your future self instructions on what to do when this day comes. Include this letter with your other important documents and share with your trusted children and advisors. Then do your best to follow this advice when they remind you of it, since you will not likely be self-aware enough of your diminished mental capacity when that time comes.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent registered investment advisory and wealth management firm specializing in retirement, tax, and investment planning. This article adapted with permission from Dimensional Fund Advisors. Kevin can be reached by calling (330)777-0688 or by email at kkroskey@truewealthdesign.com.