by Kevin Kroskey, CFP, MBA

In past articles I discussed problems with bond mutual funds and the benefits individual bonds can provide to investors. Last month I discussed why I believe the municipal bond market fears are overblown and how the fear has created a favorable risk and return profile for high quality municipal bonds. This month we’ll build upon these and discuss how to integrate individual bonds into your financial planning to create and maximize income.

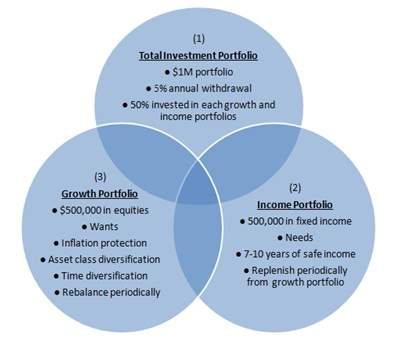

Needs and Wants

When you look at your personal expenses, some of what you spend is on things you need while other spending is on things you want. The things that you need should have very safe investments tied to these goals to meet their cash flows. These safe investments would generally be fixed income instruments such as cash, CDs, money market funds, and high-quality bonds. The things you want can have more uncertainty with the investments tied to reach these goals being more equity oriented.

When you look at your personal expenses, some of what you spend is on things you need while other spending is on things you want. The things that you need should have very safe investments tied to these goals to meet their cash flows. These safe investments would generally be fixed income instruments such as cash, CDs, money market funds, and high-quality bonds. The things you want can have more uncertainty with the investments tied to reach these goals being more equity oriented.

Most people cannot afford to direct all of their investment assets into fixed income instruments. Doing so exposes a retiree to a great amount of inflation risk and will severely harm their purchasing power and lifestyle over time. A married, non-smoking couple age 62 on average needs to plan to provide income for a spouse for 30 years, based on their joint life expectancy. Given this, becoming too conservative too quickly is likely a safe way to have money run out before you do, particularly in today’s low interest rate environment.

Rather than investing all or most of your investment assets in fixed income as you approach or enter retirement, by dedicating safe income to the things you need for a seven to ten year time period generally makes more sense. This allows the growth portfolio time to grow in order to replenish the income portfolio while also providing for your wants. Time also allows your growth portfolio to work through any market declines, which generally last a few months to no more than about three years.

Segmentation of your needs and wants to correlate to your income and growth portfolio not only works financially but also behaviorally. Investors can clearly see that even if a market decline happens, their needs are taken care of for seven to ten years. Knowing exactly where you income is coming from after you decide to stop working is a key emotional benefit that should not be underestimated. This in turn better allows the investor the mental fortitude to not sell out of the growth portfolio during a market decline and lock in losses.

If your financial planning gets too far off course and the growth portfolio doesn’t have sufficient assets to allow you to do everything you want to do, while perhaps undesirable, it nonetheless provides a model for you to evaluate these spending decisions. Doing so will better allow you to preserve your longer term financial well being and meet your needs well into the future.

This is how responsible people behave in real life: they spend money first on the things they need and if there is not extra, they cut back on the things they want but don’t necessarily need.

Utilizing Bond Ladders

After you have delineated your expenses into needs and wants, cash flows from your needs are matched to the cash flows provided by individual, high-quality bonds. These cash flows will be met by both interest payments from the bonds as well as the bonds maturing and repaying their principal value.

The easiest way to conceptualize this is to consider a zero coupon bond example. As the name implies, this type of bonds pays no interest. Instead it is purchased at a discount to principal value, which is returned upon maturity. So if you need $50,000 for your needs in your first year of retirement, which you plan to commence in five years, you could purchase a zero coupon bond today for $43,000 to receive $50,000 in five years.

This process is then repeated for each successive year in retirement with an assumed rate of inflation applied to the needs. The longer term bonds generally pay a higher rate of interest than the shorter term bonds. As you replenish your income portfolio and bond ladder over time from your growth portfolio, you are purchasing longer term bonds and continually increasing the return on your income portfolio.

It is important to note that this type of bond ladder is distinctly different than those most commonly utilized. Most bond ladders are spread equally over some period of time and are often purchased just to get the highest yield without any regard to when the investor actually will need the cash flows. This is suboptimal. The bond ladder must be designed to meet the cash flows of the investor when needed.

Implications for Investors

Most investors do not have a clear cut strategy for providing income in and throughout retirement. With interest rates near zero today, providing lifestyle-sustaining income is quite challenging. Segmenting expenses into needs and wants and then utilizing individual, high-quality bonds to meet the cash flows for your needs is a safe way to create and maximize your income while providing emotional benefits to help you stay disciplined to reach your longer term goals.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and businesses with their overall wealth management, including retirement planning, tax planning and investment management needs.