Have you acquired stock over time and seen it significantly rise in value over time? Perhaps you simply bought and held, were gifted shares, inherited stock through a credit shelter trust, or accumulated company stock through grants or options. Now you have large, unrealized capital gains and a concentrated portfolio.

What should you do? Let it ride? Or should you sell, pay taxes, and reinvest in a more diversified portfolio?

In Parts 1 and 2, we examined the issues with having a concentrated portfolio and the benefits of a more diversified one. Case studies showed selling the position, paying taxes, and investing after-tax proceeds into a diversified portfolio can vastly improve your expected, after-tax wealth. This was true whether you plan to use the money during your lifetime or if left to heirs where gains go away (cost basis stepped-up) at death.

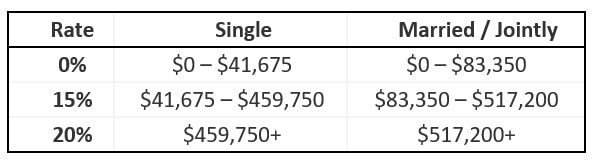

Here we’ll look at strategies to improve your transition to a more prudent portfolio. First, keep in mind your applicable tax rate. For long-term capital gains in 2022, the federal tax rates applied to taxable income levels are shown in the table below. A 3.8% Net Investment Income Tax would also apply to gains if modified adjusted gross income (MAGI) is over $200,000 (single) or $250,000 (married/jointly). State taxes may also be applicable.

Gifting

If you are charitable, appreciated stock is an ideal gift. A gift of stock allows you a tax deduction at market value, and neither you nor the charity will pay taxes once the investment is sold. You can make an outright gift to the charity today or utilize a donor-advised fund (DAF) to direct the funds over time.

Suppose you give $10,000 yearly to a variety of charities. Perhaps you donate $100,000 of stock to the DAF and receive an immediate tax deduction. You can then diversify within the DAF and dole out the $10K yearly from the DAF. This bunching strategy not only helps you deal with the concentrated stock issue but also allows you to optimize your tax deductions.

Or if your charity is within your family, rather than giving cash, gift shares to family members in lower tax brackets than you. Shares can be transferred in-kind from your account to theirs with your cost basis carrying over to them. They can then sell the shares at their tax rate.

SMAs / Tax-loss Harvesting

Think of a separately managed account or SMA as your custom-built mutual fund or ETF. By owning the stocks directly compared to owning within a mutual fund or ETF, you can utilize stock volatility to your tax advantage.

Consider the return of the S&P 500 index in 2020. The index produced a solid 18.4% return for the year. However, more than one-third of the stocks within the index posted negative returns, and fifty companies were down more than 25%. These losses can be harvested continuously and used to offset gains from your concentrated, low-basis position. Then new cash can be reinvested into a more diversified manner.

Spreading / QOZs

As seen from the tax tables, rates increase with higher incomes. Consider selling enough of your concentrated stock in a year to avoid higher rates. This may be not exceeding MAGI thresholds to prevent an additional 3.8% tax bump or make sure you avoid the 20% capital gains tax rate in a given year. But come next year, you again sell stock to target amounts and continue the process of diversifying in a tax-efficient manner over time.

Another strategy that can help with spreading but offers additional benefits is Qualified Opportunity Zones or QOZs. They were created by the Tax Cuts and Jobs Act of 2017 and generally consist of real estate investments in specified areas.

Suppose you sell stock and realize a $100,000 gain. But you then invest the proceeds into a QOZ fund. The gains are deferred until as late as 2026. Plus, if you hold the fund for ten years, any gains realized from the investment in the QOZ fund will be tax-free.

All of these strategies and more may be combined to put the odds of investment success more in your favor, doing so in a tax-efficient manner.

See Also:

Should I Sell a Stock with a Large Taxable Gain? (Part 1) – True Wealth Design

Should I Sell a Stock with a Large Taxable Gain? (Part 2) – True Wealth Design