Value and growth both sound great. What investor would not want a good value? Of course, we want growth too! These investing styles have become cemented into investing dialogue over the last 25 years but many investors still do not understand what they are.

Growth and Value

A 1987 study entitled, “In Search of Excellence: The Investor’s Viewpoint,” by investment analyst Michelle Clayman somewhat surprisingly found that good companies tend to make not so great investments compared to unexcellent companies. The idea for this study originated from the 1982 best-seller In Search of Excellence by Tom Peters and Bob Waterman. The book awarded companies an “excellent status” by virtue of their profitability, employee satisfaction and overall good working conditions. Clayman’s criteria for unexcellent companies included those with terrible profitability and “Dark Ages” management. Examples of excellent companies included powerhouses such as Johnson and Johnson, Intel, Merck, and Disney. Unexcellent companies were made up of companies like U.S. Steel, American Motors, Westinghouse, and Woolworth.

Clayman found that the unexcellent companies showed significantly greater returns over the five years following the book’s writing than their healthier counterparts. Over this time, the unexcellent companies earned investors a 298% total return while the excellent companies earned only a 182% total return. The two portfolios had almost identical levels of volatility, so what made the unexcellent portfolio deliver such higher returns to its investors?

The counterintuitive nature of this discrepancy can be explained by analogy. Similar to individuals who approach banks for loans, borrowers with strong credit (growth companies) will receive loans with lower interest rates than that of a riskier borrower. Unexcellent (value) companies end up paying borrowing higher costs in exchange for their higher risk. From an investor’s viewpoint, this translates to a lower stock price relative to their value and a higher expected return for investing in companies that are perceived as riskier.

Recent Performance

Later empirical evidence further showed that value stocks tend to outperform growth stocks over time by one to two percent yearly. However, there is no free lunch in investing, and value stocks underperformed growth stocks by a material margin in the US in 2015 and over prior three and five year periods. A short history lesson can put this in perspective.

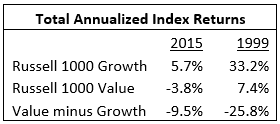

As many growth stocks and technology-related firms soared in value in the mid- to late 1990s, value strategies delivered positive returns but fell far behind growth in the relative performance race. At year-end 1998, value stocks had underperformed growth stocks over the previous 1, 3, 5, and 10 year periods. In 1999, growth stocks shone even brighter as value trailed by the largest calendar year margin in the history of the Russell indices—over 25. To many investors, it seemed foolish for money managers to hold “old economy” stocks like Caterpillar while “new economy” stocks like Yahoo! Inc. appeared to be the wave of the future.

As many growth stocks and technology-related firms soared in value in the mid- to late 1990s, value strategies delivered positive returns but fell far behind growth in the relative performance race. At year-end 1998, value stocks had underperformed growth stocks over the previous 1, 3, 5, and 10 year periods. In 1999, growth stocks shone even brighter as value trailed by the largest calendar year margin in the history of the Russell indices—over 25. To many investors, it seemed foolish for money managers to hold “old economy” stocks like Caterpillar while “new economy” stocks like Yahoo! Inc. appeared to be the wave of the future.With value stocks falling so far behind in the relative performance race, it seemed plausible that value stocks would need a lifetime to catch up, if they ever could. It took less than a year. The reversal was dramatic. Over the period April 2000 to February 2001, value stocks outperformed growth stocks by 39.7%. By February 2001, value stocks had outperformed growth stocks over the previous 1, 3, 5, and 10 year periods.

As I write this article on February 13, 2016 value stocks are up compared to growth by more than 6% so far this year. Perhaps the strong reversal is in effect. Only time will tell.

Moral of the Story

Prices are difficult to predict at either the individual stock level or the asset class level. Dramatic changes in performance can take place in a short period. While there is a sound economic rationale and empirical evidence to expectation that value stocks will outperform growth stocks over longer periods, value can underperform over any given period. If the underlying investment strategy is sound, historical results reinforce the importance that discipline is required to reap its expected rewards.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.