When taxes are computed, they are done so twice: in the regular tax system and in the Alternative Minimum Tax (AMT) system. You pay the higher of the two. Understanding how these systems work and your marginal tax rate – the tax rate on the next dollar of income – can actually turn being in the AMT into an attractive planning opportunity for high-income taxpayers.

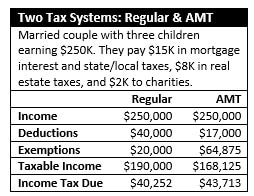

The US income tax system is progressive with higher tax rates at higher income levels. The regular tax system rates start at 0% and increases to 10%, 15%, 25%, 28%, 35% and 39.6%. The AMT disallows many deductions the regular system allows and has different exemption amounts with tax rates of 26% and 28%. Of particular note to Ohioans, is that state and local income taxes, which may be sizable, are disallowed under the AMT. Thus, high-income Ohians are more likely to find themselves in the AMT.

As income increases, deductions and exemptions are phased-out under both systems. This phase-out and the interplay of the two systems create a picture of income tax rates that looks more like mountains and valleys rather than a simple, progressive stair-step. It is important to understand the marginal tax rate throughout the mountains and valleys to identify and capitalize on tax saving opportunities.

Suppose you find yourself in the 28% AMT bracket: though in the 28% bracket, your marginal rate is typically 35% for incomes roughly from $300K to $500K. This is due to the AMT exemption being phased-out.

However, as income goes even higher, the marginal rate drops to 28% for the next several hundred thousand dollars of income before the regular tax system and the 39.6% rate applies. This 28% valley may be a sweet spot for high-income taxpayers.

Sweet Spot Saving Examples

John and Jane are married, and John is an executive earning $500K. John intends to work a few more years before retiring. In retirement, they will receive pension, deferred compensation, and Social Security payments totaling more $250K annually plus additional income from required minimum distributions (RMDs). Their marginal tax rate in retirement is likely to be 35%.

John and Jane are married, and John is an executive earning $500K. John intends to work a few more years before retiring. In retirement, they will receive pension, deferred compensation, and Social Security payments totaling more $250K annually plus additional income from required minimum distributions (RMDs). Their marginal tax rate in retirement is likely to be 35%.Their advisor completed a tax projection for the current year and found that they are in the AMT sweet spot with the next $100K of their income to be taxed at a 28% rate before climbing to a 39.6% rate under the regular tax system. The advisor recommended they realize an additional $100K of income by converting $100K from a traditional IRA to a Roth IRA. Tax savings will be the difference between the 35% future rate and 28% current rate on the $100K or $7K in tax savings over time. Tax savings can be increased even more by using and advanced Roth IRA conversion strategy, and the lower RMDs in the future may also help alleviate higher Medicare premiums.

James is single and has multiple, related businesses that are rapidly growing and highly profitable. His advisor completed a current-year tax projection and found that James can realize $300K of income in the AMT sweet spot. James’ business and income are expected to grow substantially in the next years and a 39.6% rate likely to apply. Through a combination of deferring expenses and accelerating revenue, James realizes an additional $300K of income in the current year at the 28% sweet spot rate. His tax savings will be $35K, which is the difference between the 28% and 39.6% tax rate on the $300K of income.

In summary, general advice is to defer income when income is high and accelerate income when income is low. However, the key to tax planning is to first understand your current marginal tax rate and then compare that to rates that are likely in the future. Doing so may reveal opportunities like the AMT sweet spot that seem counterintuitive but could become extremely valuable to maximize your after-tax wealth.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.