Some financial salespeople tout annuities as a better way to protect and grow your money. They’ll often say things like ‘no cost’ or ‘stock-market-like returns’ neither of which are true. Even smart people can get caught up in the hype. This article will shed light on how they really work and what you can expect from them.

Types of Annuities

There are several types of annuities. They can be categorized broadly into immediate or deferred. Immediate annuities are like a pension. You give an insurance company a lump sum, and they will provide you an income stream over time. Deferred annuities start simple being CD-like, called “fixed annuities,” but quickly get complex as you enter variable or fixed-indexed annuities.

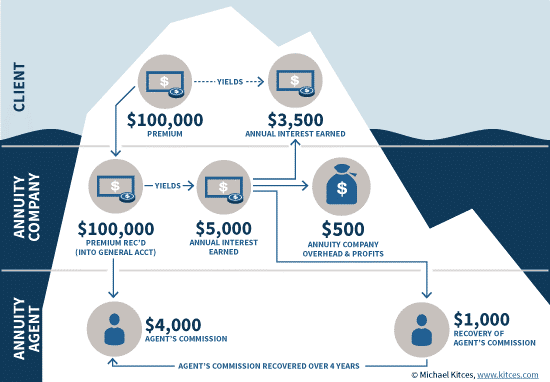

For fixed annuities, money you put into the annuity is invested into the company’s general account—mostly bond investments. Costs and profits are subtracted from the annuity company’s gross returns on their general account investments in the form of an interest rate spread. The balance is paid to the investor, which is also called the insurance company’s “cost of money.” The graphic shows an example of a 4-year annuity.

An added flair is called a fixed-indexed annuity. Here some money is used to purchase options linking the annuity to an index like the S&P 500. While this does increase upside potential, it also introduces more complexity. To the insurance company’s benefit, there are also more ways to increase profits and control their risk in having asset-based fees, caps, or spreads, all of which may be variable subject to minimum guarantees.

Real Life Example

American Equity is a publicly-traded insurance company that focuses almost solely on fixed and fixed-indexed annuities. Legally they must accurately represent the company to shareholders, and their annual report is thus quite telling on how these products really work.

From their 2017 annual report, you can see their general account yielded a 4.46% return. They kept 2.72% for themselves—operating costs, including agent commissions are also paid from this—in the form of an investment spread. Net the two above and you get their “cost of money” was 1.74%, which is about what they paid to annuity contract holders.

Even more telling is this from page 21 of the annual report: “In response to this persistent low interest rate environment, we have been reducing policyholder crediting rates for new annuities and existing annuities since the fourth quarter of 2011. We continue to have flexibility to reduce our crediting rates if necessary and could decrease our cost of money by approximately 49 basis points if we reduce current rates to guaranteed minimums.” The report goes on to say about indexed annuities on page 49, “By modifying caps, participation rates or asset fees, we can limit option costs to budgeted amounts.”

The insurance agent trying to sell these or marketing brochures they provide don’t tell you the above. But this is the truth on these fixed annuity products straight from the company’s mouth. There is no financial alchemy here. They are no silver bullet.

The insurance company investments money in bonds, keeps some of the earnings for themselves, and gives you the rest. They may induce you with up-front bonuses, attractive marketing brochures, or hypothetical income account values and purported higher retirement income (more on this in next month’s article). Yet, no matter how you slice it, you will end up with bond-like returns over time.

Or said even more simply: as my grandmother always told me, there are only 100 pennies in a dollar. The more of those pennies go to someone else, the less go to you.