One of the most interesting areas of financial research these past ten years has come, oddly, not from economists or investment researchers, but psychologists, who are pioneering a branch of study known as “behavioral finance.” This has led to one of the strangest sights in the history of Nobel prizes: the 2002 prize in economics handed out to psychologist Daniel Kahneman for, according to the Nobelprize.org website, “having integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty.”

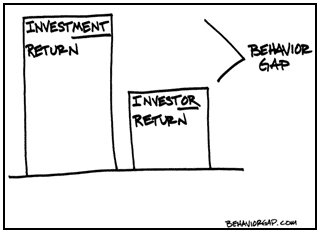

In terms of investing, there are several behavioral biases working often odds with rationality in an investor’s mind. These biases tend to culminate in the net effect that investments work better than investors. These results have been well documented by academics and investment research firms Dalbar and Morningstar for years. In fact Morningstar now reports both “Total Returns” and “Investor Returns” for most mutual funds on their website. Yet, lesser know are the ways behavioral-finance designed decisions are making their way farther and farther into our daily lives.

Behavioral finance research tells us that most people take mental shortcuts to arrive at decisions, and some of them lead to odd conclusions. Around the time you made your New Year’s resolution to lose weight, did you buy a $500 annual membership to a gym or opt for a $10 per visit pay-as-you-go fee? Most people who choose the former end up actually going to the gym less than once a month; the flat fee is only a bargain when you assume that the bold post-resolution intention will actually happen, but it’s often a terrible deal when a person’s actual behavior is taken into account.

Behavioral finance research tells us that most people take mental shortcuts to arrive at decisions, and some of them lead to odd conclusions. Around the time you made your New Year’s resolution to lose weight, did you buy a $500 annual membership to a gym or opt for a $10 per visit pay-as-you-go fee? Most people who choose the former end up actually going to the gym less than once a month; the flat fee is only a bargain when you assume that the bold post-resolution intention will actually happen, but it’s often a terrible deal when a person’s actual behavior is taken into account.

This research has been finding its way into the hands of policy makers, who are pioneering a new governmental role of protecting you against the dangers of your own mental shortcuts. One recent example is automatic enrollment in a company retirement plan. Research shows that if people are required to affirmatively opt-into having a portion of their paycheck sent to their 401(k) retirement plan, they will do so at a lower rate (67%) than if they are enrolled by default and have to affirmatively opt-out (77%). The U.S. government has been encouraging auto-enrollment policies at American corporations, on the theory that workers will be better off if more of them are making regular 401(k) plan contributions.

Another example can be seen from the city of Copenhagen. When the city painted green footprints on the sidewalks leading to litter bins, littering decreased by 46%.

The idea of applying behavioral economics to political and social initiatives sounds a lot like manipulation to its critics, who worry that we are moving toward a “nanny state” where the government feels compelled to protect us from our own behavioral biases. Reducing litter on the streets of Copenhagen is relatively noncontroversial, but what about initiatives that try to influence buyers to select more energy-efficient cars? Or government policies that discourage the consumption of certain foods or beverages? The New York City ordinance against large soda containers was based on the assumption that people were unable to recognize, on their own, the health risks of soda consumption.

Interestingly, at least one of these behavioral initiatives is now showing evidence of backfiring. The Center for Retirement Research at Boston College found that companies that have switched to automatic enrollment in their 401(k) plans have been paying for the additional cost by giving their employees smaller employer matches–3.2%, compared with an average 3.5% for plans without automatic enrollment. At the same time, the Boston College researchers and the Vanguard organization have found that for some workers, the automatic savings rate offered in the default is lower than what many workers would have chosen if they had made an affirmative decision to participate.

Only time will tell how policy makers will continue to frame the decisions we need to make and whether the change will be a net positive. Educating yourself on behavioral biases – and yes you have them – can better equip you to make decisions not only with your investments but throughout your daily life.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent, local wealth management firm and resides with his family in Bath Township.