“Managed futures” also known as “trend following” is an investment strategy that have historically achieved strong performance in both up and down markets, exhibiting low correlation to traditional stock and bond investments. It was one of the few strategies that performed well during Black Monday in 1987, through the tech wreck in the early 2000s, and in 2008 as most traditional investments suffered greatly.

Why Managed Futures?

Managed futures strategies have been around since the early 1970s. They are comprised of futures contracts that gain exposure to underlying stock, bond, currency, and commodity markets. What is different about them from traditional investments in the same markets is that they are momentum-based and attempt to identify and profit from shorter-term price trends. Momentum is well documented in academic research. It is one of the four main risk factors – the market factor, value factor, and small factor being the other three – that explain the sources of investment returns over time.

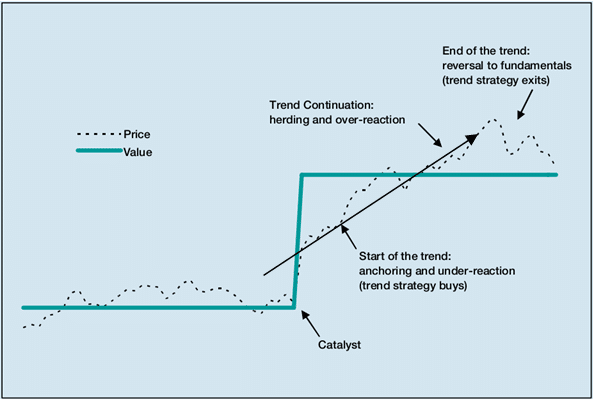

Why do markets exhibit momentum? While it is not possible to empirically test for the underlying cause of momentum, many believe investor behavior causes momentum. One of the best known of these behavioral biases is “anchoring,” or the tendency for investors to hold to views and slowly adjust to new information. This friction can cause prices to under-react to news and cause the beginning of a trend as the market price moves toward the new value. Another bias is the “herding effect” – jumping on the bandwagon late in the game after prices have moved in one direction for a while, which may cause trends to  continue, become over-extended, and in the extreme create bubbles.

continue, become over-extended, and in the extreme create bubbles.

The strategy is simple at its core: buy assets that are rising in price and sell assets that are declining. The direction of the price change does not matter; rather just that a strong trend exists. Contrast this with traditional investments in any of these markets that typically are more long-term in nature and profit only if the price increases.

Several studies document the value of managed futures as a long-term diversifier with a very low correlation to stocks, bonds and other investments. These studies also show strong evidence of the ability to identify market downturns and take short positions, which has given managed futures the edge during times of extreme stock market stress. That happened in 2008, when managed futures returned 18%, according to Morningstar, compared with a 37% drop for the Standard & Poor’s 500 index. During the “lost decade” for stocks between 2000 and 2009, managed futures cumulatively earned 13% while the S&P 500 suffered a cumulative loss of -9%.

Implementation Considerations

Managed futures is not an asset class to own for the uniformed or impatient investor, and careful consideration is required to select an appropriate managed futures fund and to fit it into or out of your investment allocation as conditions warrant.

Managed futures are active by definition. They require substantially more buying and selling in their attempt to profit from shorter-term trends. This level of trading tends to create a few hurdles. First, expense ratios of the funds (explicit costs) are high –  approaching 2% for the category average according to Morningstar. Second, the high level of trading creates expenses within the fund (implicit costs) and on top of the expense ratio that need to be monitored and properly managed by the fund. Third, the funds are tax-inefficient and should generally be placed inside tax-deferred accounts.

approaching 2% for the category average according to Morningstar. Second, the high level of trading creates expenses within the fund (implicit costs) and on top of the expense ratio that need to be monitored and properly managed by the fund. Third, the funds are tax-inefficient and should generally be placed inside tax-deferred accounts.

Considering these implementation hurdles, better options within the category include AQR’s Managed Futures Strategy (AQMIX), which has an expense ratio of 1.23% but a $5M purchase minimum. Another alternative is the WisdomTree Managed Futures Strategy ETF (WDTI) with an expense ratio of 0.95% and no minimum purchase. In 2013 and 2014, these funds have returned 9.40% and 9.69% for AQMIX and 2.95% and 5.01% for WDTI.

It is also very important to consider when the managed futures strategy will likely do well and not do well and adjust your portfolio allocation accordingly. It does best when markets exhibit persistent trends, when they are going from good to great or bad to worse. However, if the market lacks clear trends or has had sharp reversals, trend following does not work as well.

Since 2009, there have been sharp reversals across a number of markets, and those markets have been more highly correlated to each other than they have been in the past, which precludes independent trends from developing. Cumulatively from 2009 through 2013, managed futures lost -13% while the S&P 500 climbed 128%.

Markets are now trading more independently most likely due to the declining influence of the Fed following various measures of quantitative easing. In 2014, with the very strong trends of the U.S. dollar appreciating and energy prices declining, many managed futures funds turned in double-digit returns.

Coupling these market conditions with the U.S. equity market trading at lofty valuations and the fact that bonds at today’s low yields are not the safe-haven and risk-reducer they were when yields were higher, a solid managed futures strategy is worthy of careful inclusion in your portfolio to help offset risk.

Kevin Kroskey, CFP®, MBA is President of True Wealth Design, an independent investment advisory and financial planning firm that assists individuals and families with their overall wealth management, including retirement planning, tax planning and investment management needs.